7 Rules Every Stock Market Investor Should Follow

The stock market is often described as a “wealth-building machine,” and historically, that is exactly what it is. Over the last century, the stock market has provided average annual returns of roughly 10%, outperforming almost every other traditional asset class. However, in the world of 2026, the market moves faster than ever. With high-frequency trading, AI-driven algorithms, and the 24/7 noise of social media, it is easy for a beginner to get swept away in the chaos.

Investing isn’t about being the smartest person in the room; it’s about being the most disciplined. Success in the market is $20% head knowledge and $80% behavior. To help you navigate the waves of volatility and reach your financial goals, we have outlined the 7 fundamental rules that every investor—whether a novice or a pro—should follow to build lasting wealth.

1. Prioritize Time in the Market Over Timing the Market

The most common mistake beginners make is trying to “wait for the perfect moment.” They wait for the market to dip, or they wait for the election to end, or they wait for the economy to “stabilize.” The truth is that the market is never stable, and the “perfect moment” was yesterday.

The Mathematics of Delay

In investing, your greatest asset isn’t your money—it’s your time. Because of compound interest, the dollars you invest in your 20s are worth significantly more than the dollars you invest in your 40s.

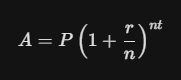

Consider the compound interest formula:

The variable that has the most impact is t (time) because it sits in the exponent. If you miss the market’s ten best days over a twenty-year period, your total returns could be slashed by as much as 50%. Since those “best days” almost always follow the “worst days,” staying invested through the downturns is the only way to capture the upside.

2. Diversify Your Portfolio to Neutralize “Single-Point” Failure

You’ve likely heard the advice: “Don’t put all your eggs in one basket.” In the stock market, this isn’t just a suggestion—it is a mathematical necessity. Diversification is often called the “only free lunch” in finance because it allows you to reduce risk without necessarily sacrificing your expected returns.

Beyond Just Owning Different Stocks

True diversification isn’t just about owning ten different tech stocks. If you own Apple, Microsoft, Nvidia, and Google, and the tech sector crashes, your entire portfolio will bleed. Real diversification means spreading your capital across:

-

Asset Classes: Stocks, bonds, real estate (REITs), and cash.

-

Sectors: Healthcare, Energy, Consumer Staples, Technology, and Utilities.

-

Geographies: Don’t just invest in the United States; look at Emerging Markets and developed international economies.

For the average investor, the easiest way to achieve this is through a Total Stock Market ETF or an S&P 500 Index Fund, which instantly gives you a piece of hundreds of different companies.

3. Master Your Emotions: The Battle Against Fear and Greed

The stock market is a device for transferring money from the impatient to the patient. Your biggest enemy as an investor isn’t the Fed, the economy, or the “Big Banks”—it is the person in the mirror.

The Psychology of Loss Aversion

Behavioral finance shows that the pain of losing $1,000 is twice as intense as the joy of gaining $1,000. This “Loss Aversion” causes beginners to panic-sell during a normal market correction.

Successful investors develop a “Mechanical Mindset.” They view market drops as a “sale” rather than a disaster. As Warren Buffett famously said: “Be fearful when others are greedy, and greedy when others are fearful.” If you find yourself checking your brokerage app ten times a day and feeling anxious, you are likely too emotionally attached to your capital.

4. Keep Your Investing Costs and Fees as Low as Possible

In the long run, fees are the “silent killer” of wealth. Many beginners ignore a 1% or 2% management fee, thinking it’s a small price to pay for professional help. However, when compounded over 30 years, that fee can consume nearly half of your total portfolio value.

The Impact of Expense Ratios

When you buy a fund, check the Expense Ratio.

-

Active Mutual Funds: Often charge 1% or more.

-

Passive Index Funds: Often charge as little as 0.03%.

On a $100,000 portfolio growing at 7%, a 1% fee will cost you over $200,000 in lost gains over 30 years compared to a low-cost index fund. In 2026, there is almost no reason to pay high commissions or management fees for a basic investment strategy. Every dollar you don’t pay in fees is a dollar that stays in your account to compound.

5. Understand Exactly What You Are Buying (Do Your Due Diligence)

“Invest in what you know” is a classic rule for a reason. Beginners often buy a stock because they heard about it on a podcast or saw a “fin-fluencer” touting it on social media. This is known as “Investing by Proximity,” and it is a fast track to losing money.

The “Elevator Pitch” Test

Before you buy a stock, you should be able to explain to a 10-year-old:

-

How the company makes money.

-

Why it will be more valuable in 10 years.

-

Who its main competitors are.

If you can’t explain the business model in three sentences, you aren’t investing—you’re speculating. You don’t need to know everything about every company, but you should understand the Fundamentals (Earnings, Revenue, Debt) of the companies you choose to own.

6. Maintain an Emergency Fund (Don’t Invest Rent Money)

This is a “boring” rule, but it is the most important for your financial survival. You should never invest money in the stock market that you might need for living expenses in the next three to five years.

Liquidity and Desperation

The stock market is volatile. If you invest your rent money and the market drops 20% right before the 1st of the month, you are forced to sell your shares at a loss to pay your bills. This is how “temporary” market fluctuations become “permanent” financial losses.

The Golden Rule: Keep 3 to 6 months of living expenses in a High-Yield Savings Account (HYSA) before you put a single dollar into the stock market. This “Cash Cushion” allows you to be an aggressive investor because you know your survival isn’t tied to the daily ups and downs of the S&P 500.

7. Automate Your Investing and Rebalance Regularly

Consistency is the secret sauce of the wealthy. Most people try to “find the money” to invest at the end of the month after they’ve paid for everything else. This rarely works.

Pay Yourself First

Set up an automatic transfer from your bank to your brokerage account the same day you get paid. This is known as Dollar-Cost Averaging. By buying every month, you automatically buy more shares when prices are low and fewer when prices are high.

The Art of Rebalancing

Once a year, you should look at your “Asset Allocation.” If your goal was to have 80% stocks and 20% bonds, but the stocks did so well that they are now 90% of your portfolio, you should sell a little bit of your “winners” and buy more of your “losers” (bonds). This forces you to sell high and buy low without having to predict the future.

Bonus: The Rule of Taxes and Retirement Buckets

To truly succeed in the stock market, you have to think about your “Silent Partner”: the government. No matter how much you make, it only matters how much you keep.

Utilize Tax-Advantaged Accounts

In the United States, utilizing accounts like a 401(k) or a Roth IRA is non-negotiable.

-

Traditional 401(k): You save on taxes today.

-

Roth IRA: You pay taxes now, but your money grows and is withdrawn 100% tax-free in retirement.

If you are investing in a standard taxable brokerage account before you have maxed out your tax-advantaged retirement “buckets,” you are essentially giving away free money to the IRS.

The Path to Wealth is Boring

If your investing is exciting, you’re probably doing it wrong. Successful investing is like watching paint dry or grass grow. It’s a series of small, disciplined, and often “boring” decisions made over the course of decades.

By following these 7 Rules, you remove the guesswork and the stress from the process. You stop being a “trader” who reacts to the news and start being an “investor” who builds a legacy. The 2026 market will have its crashes and its booms, but if you have a diversified portfolio, low fees, and a long-term horizon, you are mathematically positioned to win.

Start today, keep it simple, and let time do the heavy lifting.