What No One Tells You About Investing

The world of investing is often painted in two extremes. On one side, you have the “suit-and-tie” Wall Street types using jargon like asymmetric risk and quantitative easing to make it sound like rocket science. On the other side, you have the “Lamborghini-driving” influencers on social media promising you a 1,000% return on a new crypto coin by next Tuesday.

The truth? Both sides are selling you a version of the story that benefits them.

Investing is the most powerful tool for human freedom ever created, but it is also a psychological minefield. Most people enter the market with the wrong expectations, the wrong timeline, and a fundamental misunderstanding of how wealth is actually created. In this comprehensive guide, we are pulling back the curtain on the things no one tells you about investing.

Investing is a Test of Character, Not a Test of IQ

The most common misconception is that you need to be a “math genius” to succeed in the stock market. In reality, some of the smartest people in history—including Sir Isaac Newton—have lost fortunes in the market.

Investing is about temperament. It is about the ability to stay calm when everyone else is panicking and to stay disciplined when everyone else is getting greedy. As legendary investor Benjamin Graham said: “The investor’s chief problem—and even his worst enemy—is likely to be himself.”

The Battle of the Brain

Our brains were evolved for survival on the savannah, not for trading index funds. When the market drops 10%, your amygdala (the brain’s fear center) triggers a “fight or flight” response. No amount of IQ can save you if you don’t have the emotional control to stop yourself from hitting the “sell” button at the bottom of a crash.

The “Waiting Room” Effect: Why the First Decade Feels Like a Failure

Everyone talks about the power of compound interest, but no one tells you how painfully slow it is at the beginning.

When you start investing, your contributions do 99% of the work. If you invest $500 a month and get a 7% return, after one year, you’ve earned about $230 in interest. That’s barely enough for a nice dinner out. It feels like nothing is happening. This is the “Waiting Room” of wealth.

The Mathematics of the J-Curve

The growth of an investment portfolio follows a “J-Curve.” For a long time, the line stays relatively flat, and then it suddenly goes vertical.

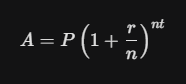

Consider the mathematical formula for compound interest:

Where:

-

A is the final amount.

-

P is the principal (your initial investment).

-

r is the annual interest rate.

-

t is the number of years.

The variable that matters most isn’t r (the return) or P (the principal)—it is t (time). Because $t$ is the exponent, it has the most dramatic impact on the final number. Most people quit in year 3 or 4 because they don’t see the “magic” happening yet. The secret no one tells you is that you have to be willing to look like you’re making no progress for a decade to become an “overnight” success in year twenty.

The Stealth Tax: How Inflation and Fees Quietly Liquidate Your Wealth

When you look at your brokerage account and see a 10% gain, you think you’ve made 10%. You haven’t. The “unspoken” truth of investing is that you are fighting a constant battle against two silent predators: Inflation and Fees.

The Inflation Hurdle

If inflation is 3% and your investment makes 7%, your “real” return is only 4%. Inflation is the rate at which your purchasing power is destroyed. If you are sitting on cash in a “high-yield” savings account that pays less than the rate of inflation, you are mathematically becoming poorer every single day.

The Tyranny of Fees

Many mutual funds and financial advisors charge an “Expense Ratio” or a management fee. It might sound small—maybe 1% or 2%. However, over a 30-year period, a 2% fee can eat up nearly 50% of your total wealth.

Let’s look at the impact of a 1.5% fee vs. a 0.1% fee on a $100,000 portfolio growing at 7% over 30 years:

-

0.1% Fee (Index Fund): Your final balance is approx. $740,000.

-

1.5% Fee (Active Fund): Your final balance is approx. $490,000.

You paid $250,000 for someone to “manage” your money, and in most cases, they didn’t even beat the market. No one tells you that the best way to get rich is often simply to stop giving your money to “experts.”

Market Volatility is the Feature, Not the Bug

New investors view volatility (the market going up and down) as a sign that something is “wrong.” They wait for the “perfect time” when the world is stable to invest.

The truth is: The world is never stable.

Volatility is the “price of admission” for the returns the stock market provides. If the market only ever went up in a straight line, there would be no risk. If there were no risk, there would be no premium (return).

Risk vs. Volatility

-

Volatility is the temporary fluctuation in price. It is the “bumpiness” of the flight.

-

Risk is the permanent loss of capital. This is the “plane crashing.”

Successful investors learn to ignore volatility and focus on avoiding risk. If you are diversified in a broad-market index fund, a 20% drop isn’t a “loss”—it’s just a sale on future shares.

Your Savings Rate Matters More Than Your Return Rate (Early On)

We spend hundreds of hours researching “the best stock” or “the best crypto,” hoping to find a way to get a 20% return instead of a 10% return.

But if you only have $1,000 to invest, the difference between a 10% return and a 20% return is only $100. However, if you find a way to save an extra $200 a month by cutting expenses or taking a side hustle, you’ve effectively increased your “return” by 240%.

The Fuel and the Engine

-

Your Income/Savings is the fuel.

-

Your Investment Strategy is the engine.

In the first 10 to 15 years of your journey, the size of your “fuel tank” matters infinitely more than how efficient your “engine” is. No one tells you that “working on your career” or “starting a side business” is often the best investment strategy you have.

The Danger of the “Financial Influencer” Echo Chamber

In 2026, we are bombarded with financial content. The problem is that social media algorithms don’t reward “safe, boring, long-term advice.” They reward “outrageous, bold, and risky claims.”

Survivorship Bias

You see a video of someone who turned $\$5,000$ into $\$500,000$ on a meme coin. What you don’t see are the 100,000 people who tried the same thing and lost their $\$5,000$. This is called survivorship bias.

Financial influencers often “curate” their wins and hide their losses. If someone is telling you to buy a specific asset, ask yourself: “Does this person benefit if I buy this?” Often, they are already “positioned” and need you to buy so they can sell.

The Mathematical Reality of Recovering from a Crash

No one tells you how much harder it is to “come back” from a loss than it is to grow. The math of percentages is asymmetrical.

If you have $100 and you lose 50%, you have $50. To get back to $100, you don’t need a 50% gain; you need a 100% gain.

| Loss | Gain Needed to Break Even |

| 10% | 11.1% |

| 20% | 25% |

| 30% | 42.9% |

| 50% | 100% |

| 90% | 900% |

This is why Downside Protection is the secret of the wealthy. It is better to miss out on a “hot” 100% gain than to get caught in a 50% crash. Wealth is built by not losing what you already have.

Why “Diversification” is the Only Free Lunch in Finance

You’ve heard the phrase “don’t put all your eggs in one basket.” But most people don’t understand the mathematical beauty of it.

In most areas of life, if you want a higher reward, you must take a higher risk. Investing is the only area where you can actually lower your risk without necessarily lowering your return. This is achieved through diversification.

By owning 500 companies (like the S&P 500) instead of one, you eliminate “Company Specific Risk.” If one company goes bankrupt, the other 499 carry you forward. The “secret” that professionals know is that you don’t need to find the “needle in the haystack”—you can just buy the whole haystack and win.

Investing Won’t Fix a Spending Problem

There is a common fantasy that if you just “hit it big” in the market, your financial problems will vanish.

The reality is that money is a magnifier. If you are bad at managing $3,000 a month, you will be catastrophic at managing $3,000,000. This is why so many lottery winners and professional athletes go broke.

Investing is a tool for wealth multiplication, but if the “base number” (your net savings) is zero or negative because of your lifestyle, then:

You have to master your defense (spending) before your offense (investing) can ever make you rich.

Knowing When to Sell is Harder Than Knowing When to Buy

Most of the “financial education” in the world is about how to start.

“Buy this ETF!” “Open this IRA!”

But no one talks about the “Exit Strategy.” When do you sell?

-

Do you sell when the market hits an all-time high? (No, because it often goes higher).

-

Do you sell when the market is crashing? (No, that’s when you should buy).

-

Do you sell when you need the money? (Maybe, but what if the market is down that year?)

The Rule of “Rebalancing”

Successful investors don’t “guess” when to sell. They use a system called Rebalancing. If your goal is to have 80% stocks and 20% bonds, and the stocks do so well that they now represent 90% of your portfolio, you sell that extra 10% and buy bonds.

This forces you to do the hardest thing in the world: Sell high and buy low. It removes the emotion and replaces it with a mechanical process.

The Quiet Path to Wealth

The “truth” no one tells you is that successful investing is incredibly boring. It’s like watching grass grow or paint dry. It’s not a thrill ride; it’s a long, disciplined march.

Wealth is built in the quiet moments. It’s built when you decide to keep your 5-year-old car and invest the “car payment” instead. It’s built when you ignore the news of a “recession” and keep your automatic transfers running. It’s built when you accept that you are not smarter than the market and decide to just “be” the market.

Stop looking for the secret coin or the hidden stock. The “secret” is right in front of you: Spend less than you earn, invest the difference in a diversified way, and let time do the work.

It’s simple, but simple is rarely easy.