Why Emotional Spending Is So Dangerous

We have all been there. You have a grueling day at the office, your boss is breathing down your neck, or perhaps you just went through a tough breakup. On the way home, or while scrolling through your phone in bed, you find yourself on a retail website. Suddenly, you’ve bought a $200 pair of shoes or a high-end kitchen gadget you’ll likely never use. For a brief moment, you feel a surge of excitement—a “hit” of pure joy.

But by the time the package arrives, the thrill has vanished, replaced by a nagging sense of guilt and a smaller balance in your savings account.

This is emotional spending. While it might seem like a harmless “guilty pleasure,” it is actually one of the most significant barriers to building long-term wealth. In the world of behavioral finance, emotional spending is viewed as a high-stakes “leak” in your financial bucket. If you don’t plug it, no amount of income or investment savvy will ever be enough to fill it.

What Exactly is Emotional Spending?

At its core, emotional spending is the act of buying things you don’t need—and often don’t even want—to manage, enhance, or suppress your emotions. It is a coping mechanism. Instead of dealing with the root cause of an emotion, we use a transaction to provide a temporary distraction.

While we often associate this with “retail therapy” during times of sadness, emotional spending happens across the entire emotional spectrum:

-

Stress: Buying convenience or luxury to compensate for a high-pressure lifestyle.

-

Boredom: Scrolling through shopping apps as a form of entertainment.

-

FOMO (Fear of Missing Out): Spending money to feel included in a social trend or peer group.

-

Celebration: Overspending because you feel you “deserve it” after a win.

The Biological Hijack: How Your Brain Forces You to Shop

To understand why emotional spending is so hard to stop, we have to look at the biology of the human brain. We aren’t as rational as we like to think. In fact, our financial decisions are often hijacked by our ancient survival instincts.

The Dopamine Loop

When you see something you want and anticipate the purchase, your brain releases dopamine, a neurotransmitter associated with pleasure and reward. Interestingly, the highest spike of dopamine occurs during the anticipation of the purchase, not the actual ownership of the item. This is why the “high” disappears so quickly after you hit the “Complete Order” button.

Amygdala vs. Prefrontal Cortex

The prefrontal cortex is the part of your brain responsible for logic, long-term planning, and financial discipline. However, when you are emotional—whether stressed, angry, or even overly excited—the amygdala (the emotional center) takes control. The amygdala prioritizes immediate relief over long-term security. In this state, your brain literally loses the ability to care about your retirement fund or your credit card interest rates.

Common Emotional Triggers That Drain Your Bank Account

Identifying the “why” behind your spending is the first step toward financial sobriety. Most emotional spenders fall into one of these psychological traps:

1. The “I Deserve It” Trap

This is common among high-achieving professionals. You work 60 hours a week, and you feel that your hard work justifies a luxury purchase. While reward is important, using it as a justification for frequent, unplanned spending leads to lifestyle inflation, where your expenses rise just as fast as your income.

2. The Boredom Gap

In the digital age, the store is always in your pocket. Boredom is perhaps the most expensive emotion in 2026. When we have a few minutes of downtime, we check social media, see an ad, and buy. It’s a mindless habit that can cost thousands of dollars a year in “micro-spending.”

3. Comparison and Social Validation

Social media has created a “Digital Joneses” effect. We see influencers or peers showing off a curated version of their lives, and we feel a sense of Relative Deprivation. We spend money to prove to the world (and ourselves) that we are successful, even if it means going into debt to do so.

Why Emotional Spending is the Ultimate Wealth Killer

The danger of emotional spending isn’t just the money you lose today; it’s the opportunity cost of what that money could have become. In finance, we call this the “Cost of the Lost Potential.”

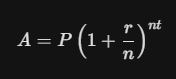

The Math of the “Small” Spree

Imagine you spend $200 a month on emotional “retail therapy.” If you instead invested that $200 into a diversified index fund with an average 7% annual return, look at the power of compound interest over time:

After 30 years, that “harmless” $200 monthly habit would have grown into approximately $244,000. By spending that money emotionally, you aren’t just losing $200; you are effectively setting fire to a quarter of a million dollars of your future freedom.

The Debt Spiral

Emotional spending is rarely done with “extra” cash. It often ends up on credit cards. When you add a 20% or 25% APR to an impulse purchase, you are paying a massive “tax” on your emotions. This creates a cycle: you spend because you’re stressed, then you get stressed because you’re in debt, so you spend more to feel better.

The “Retail Therapy” Myth: Why the High is Temporary

The term “retail therapy” is a misnomer. Therapy is designed to provide long-term healing; retail provides a temporary mask. This is due to a phenomenon known as Hedonic Adaptation.

Humans are incredibly good at getting used to new things. Whether it’s a new iPhone, a designer handbag, or a faster car, the “newness” eventually fades. Within weeks, the item that made you so excited becomes part of your background environment. This forces you to seek out a new purchase to get the same hit of dopamine. You are on a treadmill, running faster and spending more, but your level of happiness remains exactly the same.

The Social Media Effect: Comparison is the Thief of Your Savings

In the past, you only had to worry about the people on your street. Today, you are comparing your life to the top 0.1% of the entire world. Social media algorithms are designed to trigger your emotions and show you products that fit your “idealized” self.

When you see a friend on a luxury vacation, your brain doesn’t see their credit card statement or their lack of retirement savings. It only sees a “status signal.” Emotional spending often becomes a way to “perform” success for an audience that isn’t really paying attention.

How to Identify Your Personal Financial Triggers

To stop the leak, you need to become a financial detective. For the next 30 days, every time you make a non-essential purchase, write down:

-

What you bought.

-

How much it cost.

-

What you were feeling exactly five minutes before the purchase.

You will likely see a pattern. Do you shop mostly on Sunday nights (Anxiety)? Do you shop after a fight with a spouse (Anger)? Do you shop when you feel lonely? Once you name the trigger, it loses its power over you.

Practical Strategies to Stop Emotional Spending Today

Behavioral discipline is more important than mathematical skill when it comes to money. Use these “hacks” to protect your prefrontal cortex from your amygdala:

1. The HALT Method

Never go shopping (online or in-person) if you are:

-

Hungry

-

Angry

-

Lonely

-

Tired

In these states, your willpower is at its lowest, and your emotional brain is in the driver’s seat.

2. The 24-Hour (or 72-Hour) Rule

For any purchase over a certain threshold (e.g., $50), you must wait at least 24 hours. Put the item in your cart, then close the tab. This gives your brain time to move from an emotional state to a logical one. Most of the time, the “need” for the item disappears by the next morning.

3. Remove the Frictionless Buying

The easier it is to buy, the easier it is to spend emotionally.

-

Delete shopping apps from your phone.

-

Unsubscribe from marketing emails (those “24-hour flash sales” are designed to trigger your panic/scarcity emotions).

-

Remove saved credit card info from your browser. Making yourself go find your wallet to type in the numbers provides a critical “pause” to rethink the purchase.

4. Find Zero-Cost Emotional Outlets

If you shop to relieve stress, you need a different way to relieve stress that doesn’t involve your bank account. Exercise, reading, calling a friend, or even a 10-minute meditation can provide the same emotional regulation as a purchase, without the financial hangover.

Turning Emotional Spending into Emotional Investing

What if you could get that same “dopamine hit” from seeing your money grow? This is a psychological shift used by many wealthy individuals.

Instead of treating yourself to a “thing,” treat yourself to an “asset.” When you have a bad day, instead of buying something on Amazon, transfer $50 into your brokerage account or buy a fractional share of a company you admire. You still get the satisfaction of “doing something” and the thrill of the transaction, but instead of losing value, you are building your future sovereignty.

Reclaiming Your Financial Narrative

Emotional spending is not a sign of being “bad with money.” It is a sign of being human. Our brains are simply not naturally wired for the abundance and ease of modern consumerism.

However, true financial education is about more than just knowing how to pick a stock or balance a spreadsheet; it’s about self-mastery. When you stop using money to fix your feelings, you start using it to build your life.

Wealth isn’t just about having a high net worth. It’s about having the freedom to make choices that aren’t dictated by your emotions or your debt. Plug the emotional leaks today, and you’ll be amazed at how quickly your financial bucket begins to overflow.