10 ways to reduce the cost of motorcycle insurance

For many riders, the thrill of the open road is often dampened by the sting of the monthly insurance premium. Whether you’re riding a high-performance sportbike, a rugged adventure tourer, or a classic cruiser, insurance is a non-negotiable part of the journey. However, just because it’s mandatory doesn’t mean it has to be exorbitant.

In the world of 2026, insurance algorithms have become more complex than ever, utilizing everything from your credit history to your digital footprint to determine your “risk profile.” If you aren’t proactive, you might find yourself paying a “laziness tax” to your provider.

If you want to keep more money in your pocket without sacrificing the protection of your assets, here are 10 proven ways to reduce the cost of your motorcycle insurance.

1. Mastering the Art of Comparison Shopping

The single biggest mistake most riders make is accepting their renewal quote without looking elsewhere. Insurance companies operate on a model of “price optimization,” which essentially means they will charge you as much as they think you are willing to pay before you leave.

The Variance of Risk Assessment

Every insurance company has a different “appetite” for risk. Company A might hate sportbikes but love cruisers, while Company B might specialize in riders over the age of 40. This means that for the exact same bike and the exact same rider, quotes can vary by as much as 30% to 50%.

How to Execute This

Don’t just use one aggregator site. Check independent agents and direct-to-consumer websites. Aim to get at least five quotes every two years. In the digital age, this process takes less than 30 minutes but can save you hundreds of dollars annually.

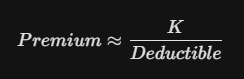

2. Leverage the Mathematical Power of High Deductibles

The deductible is the amount you agree to pay out of your own pocket before the insurance company pays for a claim. There is a direct, inverse mathematical relationship between your deductible and your premium.

The Inverse Relationship Formula

While not perfectly linear, the relationship can be simplified as:

Where $K$ represents your base risk factor. By increasing your deductible from $500 to $1,000, you are signaling to the insurer that you are willing to take on more of the “small” risks yourself. In exchange, they will often slash your comprehensive and collision premiums significantly.

The Strategy

Only do this if you have an emergency fund. If you can’t afford a $1,000 surprise expense, a high-deductible plan is a gamble. But if you have the cash, you are better off “self-insuring” for small scratches and dents while letting the insurance company handle the catastrophic losses.

3. Complete a Certified Motorcycle Safety Foundation (MSF) Course

Insurance companies love data, and the data shows that riders who take formal training are significantly less likely to file a claim. Even if you’ve been riding for twenty years, a “Refresher” or “Advanced Rider” course can pay for itself in a single year.

The “Safe Rider” Discount

Most major carriers offer a discount ranging from 5% to 15% for riders who have completed a certified safety course within the last three years.

Long-term Benefits

Beyond the immediate discount, these courses teach you low-speed maneuvers and emergency braking—skills that prevent the “minor drops” that often lead to expensive cosmetic claims. A clean claim history is the ultimate long-term discount.

4. The Multi-Policy “Bundle” Advantage

Insurance companies are in a war for “customer lifetime value.” They want to be your one-stop shop for everything. If you have your car, your home, and your life insurance with different companies, you are leaving money on the table.

The Logic of the Multi-Line Discount

When you “bundle” your motorcycle with your auto or homeowners policy, you can see a 10% to 25% reduction across the board. The insurer is willing to take a lower margin on each individual policy because the likelihood of you switching companies (churning) drops significantly once you have three or four policies tied together.

5. Invest in Security and Proper Storage

A motorcycle is far easier to steal than a car. Because of this, “Comprehensive” coverage—which covers theft—makes up a huge portion of your premium, especially in urban areas.

Garage vs. Street Storage

If you tell your insurer that your bike is stored in a locked, private garage rather than on the street or in a public parking structure, your rate will drop. Why? Because the “exposure to loss” is statistically lower.

Tech-Based Security

Modern anti-theft devices can provide additional discounts:

-

GPS Trackers: Systems that allow for recovery after a theft.

-

Disc Locks with Alarms: High-decibel deterrents.

-

LoJack Systems: Many insurers have specific, deep discounts for bikes equipped with professional recovery systems.

6. Maintain a Pristine Riding and Driving Record

This seems obvious, but many riders don’t realize that their auto driving record affects their motorcycle insurance. If you get a speeding ticket in your minivan, your Hayabusa insurance is going up.

The “Surcharge” Timeline

In most states, a single speeding ticket or a minor “at-fault” fender bender will stay on your record and affect your insurance rates for three to five years. Over that period, a single ticket could cost you an extra $500 to $1,000 in cumulative premium increases.

Pro-Tip: Defensive Driving School

In many jurisdictions, if you receive a ticket, you can take a defensive driving course to keep the “points” off your record. Always take this option. The cost of the course is a fraction of the insurance surcharge you’ll face over the next three years.

7. Optimize Your Coverage Based on Seasonal Use

If you live in a region where it snows, you probably aren’t riding in January. Paying for “Full Coverage” during months when the bike is up on stands is a waste of capital.

The “Lay-Up” Policy

Many specialty motorcycle insurers offer what is known as a Lay-Up Policy. This maintains your comprehensive coverage (for fire and theft while the bike is in the garage) but suspends the collision and liability portions during the winter months.

Usage-Based Insurance (UBI)

In 2026, “pay-per-mile” insurance is becoming standard. By installing a small device or using an app to track your mileage, you only pay for the time you are actually on the road. For weekend warriors who only ride 1,000 miles a year, this can be 50% cheaper than a traditional policy.

8. Pay Your Annual Premium in Full

It’s tempting to pay month-to-month. It feels easier on the budget. However, almost every insurance company charges a “convenience fee” or “installment fee” for monthly payments, usually ranging from $1 to $5 per month.

The Hidden Interest Rate

If your annual premium is $600 and the company charges a $5 monthly fee, you are paying an extra $60 a year. That is essentially a 10% interest rate on your own insurance.

Avoid the “Paper Fee”

Furthermore, many companies offer an “Electronic Funds Transfer” (EFT) or “Paperless” discount. By automating your payment and receiving your documents via email, you can save an additional $20 to $50 a year.

9. Choose Your Motorcycle Wisely

Before you buy a bike, call your agent. The “Insurance Group” of a motorcycle is determined by its displacement (cc), its style, and its historical “crashability.”

The “Superbike” Penalty

A 600cc supersport bike (like a Yamaha R6) is often more expensive to insure than a 1200cc cruiser (like a Harley-Davidson Sportster). Why? Because the data shows that supersport riders are statistically more likely to engage in high-speed maneuvers and file total-loss claims.

The “Standard” Sweet Spot

If you want the best performance-to-insurance ratio, look for “Standard” or “Naked” bikes. These often have the same engines as sportbikes but are classified differently by insurers, leading to significantly lower rates.

10. Improve Your “Insurance Score” (Credit Rating)

In many US states, your credit score is a major factor in your insurance premium. Insurers have found a strong correlation between financial responsibility and road responsibility.

The Logic of the Score

A rider with a high credit score is statistically less likely to file “frivolous” claims and more likely to maintain their vehicle properly.

How to Improve It

-

Pay down credit card balances: Keeping your utilization under 30% boosts your score quickly.

-

Fix errors: Check your credit report for mistakes that might be dragging your score down.

-

Consistency: Even a 50-point increase in your credit score can move you into a different “rating tier,” potentially saving you 10-15% on your motorcycle insurance.

Understanding the “Loyalty Tax”

One final thing to watch out for is the Loyalty Tax. This is a psychological phenomenon where insurance companies slowly raise rates on long-term customers, assuming they won’t go through the hassle of switching.

If you see your rate go up by 3% to 5% every year despite a clean record and no claims, you are being targeted by the “loyalty tax.” This is the market telling you it’s time to shop around.

Take the Handlebars of Your Finances

Reducing the cost of your motorcycle insurance isn’t about finding a “secret” company; it’s about understanding the variables that the companies use to judge you. By increasing your deductible, taking a safety course, and auditing your policy every two years, you can significantly lower your cost of ownership.

Don’t let high premiums keep you in the garage. Use these strategies to optimize your coverage so that every dollar you spend is going toward your protection, not the insurance company’s profit margins.