Why financial discipline matters more than income

In the world of personal finance, there is a dangerous myth that governs the lives of millions: the belief that “if I just made more money, all my problems would disappear.” We are conditioned to believe that a six-figure salary is the ultimate shield against financial stress. However, history and data show a much more complex reality. Professional athletes, lottery winners, and high-earning executives often find themselves in bankruptcy, while modest earners—teachers, janitors, and administrative assistants—frequently retire as millionaires.

The difference isn’t found in the amount on their paychecks; it’s found in their financial discipline. While income determines your potential for wealth, discipline determines your reality. In this comprehensive guide, we will explore why the “how much” matters far less than the “how,” and how you can master the habits that lead to genuine financial freedom.

The Income Trap: Why More Money Doesn’t Solve Poor Habits

Most people treat their bank accounts like a bucket with a hole in the bottom. They believe the solution is to pour more water (income) into the bucket. But if the hole (spending habits) keeps growing alongside the flow of water, the bucket will never stay full. This is the “Income Trap.”

The Reality of Lifestyle Inflation

Lifestyle inflation, or “lifestyle creep,” is the phenomenon where your expenses rise in direct proportion to your income. You get a $10,000 raise, and suddenly your current car feels outdated, your apartment feels small, and your wardrobe feels inadequate.

Without discipline, a higher income simply funds a more expensive version of the same financial struggle. You aren’t getting wealthier; you are just living a more luxurious form of “paycheck to paycheck.”

High Earners and Invisible Poverty

In the United States, a significant percentage of households earning over $100,000 a year report living paycheck to paycheck. This is “invisible poverty”—the state of having high-end assets but zero liquidity and massive debt. These individuals are one missed paycheck away from disaster. Discipline is the only tool that transforms a high income into a high net worth.

The Mathematics of Wealth: Discipline vs. Raw Earnings

To understand why discipline wins, we have to look at the math. Wealth is not a measurement of how much you make; it is a measurement of how much you keep.

The “Net Worth” Equation

Your net worth is simply Assets minus Liabilities.

-

Person A earns $250,000 a year but spends $245,000 to maintain their status. Their annual wealth growth is $5,000.

-

Person B earns $60,000 a year but lives with extreme discipline, spending $40,000. Their annual wealth growth is $20,000.

In this scenario, Person B—who earns less than a quarter of Person A—is actually building wealth four times faster. Over twenty years, Person B will be significantly wealthier and more secure. Discipline allows you to optimize the “gap” between what you earn and what you spend.

The Power of the Savings Rate

Your “Savings Rate” is the single most important number in your financial life. It is the percentage of your take-home pay that you set aside. A high earner with a 2% savings rate will always be outperformed by a moderate earner with a 20% savings rate. Discipline is what allows you to maintain that rate regardless of what your peers are doing.

Behavioral Economics: Why Our Brains Fight Financial Discipline

Humans are not naturally rational when it comes to money. We are biological creatures designed for survival, not for 401(k) management. Understanding the “bugs” in our mental software can help us build better discipline.

The Hedonic Treadmill

The “Hedonic Treadmill” is the psychological theory that people quickly return to a relatively stable level of happiness despite major positive or negative events. When you buy a new car, you get a “happiness spike.” But within weeks, that car becomes your “new normal.”

Discipline is the conscious decision to step off the treadmill. It is the realization that the next purchase won’t provide permanent satisfaction, allowing you to prioritize long-term security over temporary spikes.

Social Proof and “The Joneses”

We are social animals. In the past, being “out of step” with the tribe meant physical danger. Today, that instinct manifests as the need to match the spending habits of our neighbors and coworkers. Discipline requires the emotional maturity to be “the odd one out”—to drive the older car or live in the smaller house—because you are focused on a goal that they can’t see.

Compound Interest: The Disciplined Saver’s Superpower

Einstein reportedly called compound interest the “eighth wonder of the world.” However, compound interest is a jealous god; it only rewards those who stay the course. It requires the discipline to leave your money alone for decades.

The Cost of “Dipping In”

Many people start saving, but at the first sign of a “want”—a vacation, a new gadget, or a wedding—they liquidate their investments. This resets the “compounding clock.”

Consider two investors:

-

The Undisciplined High Earner: Saves $2,000 a month but “cashes out” every five years to buy a new car.

-

The Disciplined Moderate Earner: Saves $500 a month and never touches it for 30 years.

Even with a lower monthly contribution, the disciplined earner will likely end up with hundreds of thousands of dollars more because they allowed time to do the heavy lifting.

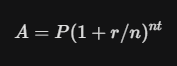

The Formula for Wealth

The formula for compound interest is:

Where:

-

A is the final amount.

-

P is the principal.

-

r is the interest rate.

-

t is the time.

Notice that Time ($t$) is the exponent. Discipline is what keeps your money in the market long enough for that exponent to work its magic.

Strategic Budgeting: The Blueprint of a Disciplined Life

You cannot have discipline without a plan. A budget is not a set of handcuffs; it is a map to your destination. It tells your money where to go instead of you wondering where it went.

The 50/30/20 Rule as a Starting Point

For those new to financial discipline, the 50/30/20 rule is an excellent framework:

-

50% Needs: Housing, utilities, groceries, basic transport.

-

30% Wants: Dining out, hobbies, Netflix, “the fun stuff.”

-

20% Financial Goals: Debt repayment, emergency funds, and investments.

Discipline is the act of ruthlessly protecting that 20% bucket. If your “Needs” creep into your “Goals,” you aren’t being disciplined.

Zero-Based Budgeting for Maximum Efficiency

If you want to take your discipline to the next level, use Zero-Based Budgeting. This means every single dollar you earn is assigned a job before the month begins. If you have $10 left over at the end of your planning, you assign it to a category (like “extra debt payment”). When your bank account shows $0 “unassigned” dollars, you have achieved total control.

Risk Management: Discipline as a Shield Against Recessions

Income can be taken away. Jobs can be lost, industries can be disrupted, and economies can crash. Discipline, however, builds a fortress that protects you during these times.

The Emergency Fund: The “Sleep at Night” Factor

A disciplined individual prioritizes an emergency fund—typically 3 to 6 months of expenses—before they start buying luxuries. This fund isn’t for “growth”; it’s for “insurance.” High earners without discipline often find themselves in total panic during a layoff because their “lifestyle” requires a massive, uninterrupted flow of cash just to stay afloat.

The Power of Low Fixed Costs

Discipline allows you to keep your “Fixed Costs” (the bills you must pay every month) low. The lower your fixed costs, the more resilient you are. If you earn $10,000 but only need $3,000 to survive, you have a $7,000 safety margin. If you earn $20,000 but need $19,000 to survive, you are in a high-risk position. Discipline is the art of maximizing that margin.

How to Develop Financial Discipline: Practical Habits for Success

If you weren’t born with the “discipline gene,” don’t worry. Discipline is a muscle that can be trained through small, consistent actions.

1. Automate Everything

The best way to be disciplined is to remove the need for willpower. Set up an automatic transfer from your paycheck directly to your savings and investment accounts. If you never see the money in your checking account, you won’t be tempted to spend it. This is “Paying Yourself First.”

2. Implement the “Wait Rule”

Impulsive spending is the enemy of discipline. Create a rule: for any purchase over $100, you must wait 48 hours. For any purchase over $500, you must wait a week. In most cases, the “must-have” feeling will fade, and you’ll realize the purchase wasn’t necessary.

3. Track Your Progress, Not Just Your Spending

Don’t just look at what you spent; look at your Net Worth. Use a spreadsheet or an app to track your total assets vs. your total liabilities once a month. Seeing that “Net Worth” number go up is a much more powerful (and lasting) reward than the dopamine hit from a new gadget.

The Role of Psychology: Finding Contentment in a Consumerist World

Ultimately, financial discipline is an internal battle. It is a fight against the constant message that “more is better.”

Practicing Gratitude

Contentment is the ultimate “financial hack.” If you are genuinely happy with what you have, marketers have no power over you. Take time each week to reflect on the things in your life that didn’t cost a dime: your health, your relationships, your skills. This reduces the emotional “hunger” that often leads to impulsive spending.

Redefining Status

In our culture, status is often signaled by what we spend. “I’m successful, look at my car.” A disciplined person redefines status by what they own. True status is the freedom to leave a job you hate, the ability to help a friend in need, or the peace of mind of having zero debt.

Income is the Engine, Discipline is the Steering Wheel

Imagine a powerful sports car with a massive engine (High Income) but no steering wheel (No Discipline). No matter how fast it goes, it will eventually crash. Now imagine a modest sedan (Moderate Income) with a perfect steering system and a clear map. It may take longer to get there, but it will reach the destination safely and reliably.

Wealth is not a prize for the highest earner; it is a reward for the most disciplined. By focusing on your habits, automating your savings, and mastering your impulses, you can build a financial life that is far more secure and rewarding than those who earn millions but keep nothing.

Stop waiting for a raise to start your financial journey. The tools for wealth are already in your hands—they are called discipline.