Should You Invest in US Stocks from Emerging Markets?

In the rapidly evolving financial landscape of 2026, the boundary between “local” and “global” has almost entirely disappeared. For investors living in emerging markets (EM)—nations like Brazil, India, Mexico, or Southeast Asian economies—the question of whether to move capital into the United States is no longer just a trend; it is a fundamental strategic decision.

The US stock market remains the largest, most liquid, and most innovative financial ecosystem on the planet. But for someone earning in a local currency and dealing with local inflation, is the leap to Wall Street worth the effort? In this deep dive, we explore the truth about international diversification, the hidden risks, and why “going global” might be the most important move for your portfolio this decade.

Why the US Stock Market is Still the “Gold Standard” for Global Capital

When we talk about the US stock market, we aren’t just talking about a country; we are talking about the command center of global capitalism. As of 2026, US-listed companies account for nearly 45-50% of the world’s total equity market capitalization.

The Innovation Monopoly

The US remains the primary hub for the most disruptive technologies. Whether it is the continued maturation of Generative AI, the commercialization of Quantum Computing, or advancements in Biotech, the leaders in these fields almost exclusively list on the NYSE or the NASDAQ. By staying solely in an emerging market, you are essentially betting against the companies that are defining the future of the global economy.

Unmatched Liquidity and Transparency

In many emerging markets, a “bad day” for a single large company or a sudden political shift can cause the entire local index to freeze or crash. The US market offers Liquidity—the ability to enter and exit positions instantly at a fair price. Furthermore, the regulatory oversight provided by the SEC ensures a level of transparency that is often lacking in less developed financial jurisdictions.

The Power of Currency Diversification: Hedging Against Local Volatility

For an investor in an emerging market, you aren’t just investing in a company; you are investing in a currency. This is perhaps the most compelling reason to hold US stocks.

The US Dollar as a “Safe Haven”

Historically, during times of global economic stress, the US Dollar (USD) tends to strengthen against emerging market currencies. If your local currency devalues by 10% against the dollar while your US stocks remain flat, you have technically increased your purchasing power by 10% in local terms.

High Growth vs. High Stability: Comparing EM and US Returns

Emerging markets are often touted for their “high growth potential.” While it is true that an EM economy might grow at 6% while the US grows at 2%, that growth does not always translate to stock market returns for shareholders.

| Feature | Emerging Markets (EM) | US Stock Market |

| Primary Driver | Commodities & Local Consumption | Global Technology & Services |

| Volatility | High (Political/Currency Risk) | Moderate (Market Risk) |

| Dividend History | Often inconsistent | Strong “Dividend Aristocrats” |

| Concentration | Often dominated by 3-5 companies | Highly diversified sectors |

The “Commodity Trap”

Many emerging market indices (like the Bovespa or the JSE) are heavily weighted toward commodities—oil, iron ore, and agriculture. These are cyclical and unpredictable. The US market, however, is driven by intellectual property and software, which traditionally offer higher margins and more consistent long-term growth.

The Hidden Risks: What Emerging Market Investors Often Overlook

Investing in the US is not a “free lunch.” There are specific hurdles that international investors must navigate to avoid losing their gains to taxes and fees.

Dividend Withholding Taxes

The US government typically imposes a 30% withholding tax on dividends paid to foreign investors. While many countries have tax treaties that reduce this to 15%, it is a “leakage” in your portfolio that you must account for.

Estate Tax (The “Death Tax”)

This is the one risk no one tells you about. If a non-US resident owns more than $60,000 in US-situated assets (stocks) at the time of their death, they could be subject to an estate tax of up to 40%.

Important Note: To avoid this, many savvy international investors use “offshore” structures or invest through Ireland-domiciled ETFs, which track the US market but are not subject to US estate taxes for foreigners.

How to Invest in US Stocks from Abroad in 2026

Technological advancements in 2026 have made it easier than ever to access Wall Street from a smartphone in Mumbai or São Paulo.

Global Digital Brokerages

Platforms have emerged that allow users to open a US brokerage account in minutes. These platforms often offer:

-

Fractional Shares: Buy $10 worth of Amazon even if the share price is $2,000.

-

Low-Cost Currency Exchange: Directly converting local currency into USD at mid-market rates.

-

W-8BEN Automation: Automatically handling the paperwork required to certify your foreign status for tax purposes.

US-Listed ETFs (The “Lazy” Success Strategy)

For most people, picking individual stocks is a losing game. The most efficient way to invest is through ETFs (Exchange-Traded Funds).

-

VOO or SPY: Tracks the S&P 500.

-

VTI: Tracks the entire US stock market.

-

QQQ: Tracks the 100 largest non-financial tech companies.

The Psychology of “Home Country Bias”

Most investors suffer from Home Country Bias—the tendency to invest the majority of their money in the country where they live. They do this because it feels “safer” or more familiar.

Why Familiarity is an Illusion

You might feel like you “know” the local bank or the local power company, but that familiarity doesn’t protect you from a local economic crisis. True safety comes from Global Diversification.

In 2026, the wealthiest individuals in emerging markets don’t keep their money in local banks; they keep it in global assets. By investing in US stocks, you are following the “Smart Money” and ensuring that your family’s future isn’t tied to the success or failure of a single local politician.

Strategic Asset Allocation: How Much Should You Move?

Should you move 100% of your money to the US? Probably not. You still have local expenses and local opportunities.

The “Core and Satellite” Approach

A common 2026 strategy for EM investors is:

-

70% Core (US/Global): Invested in broad US index funds or global ETFs to ensure long-term wealth preservation and USD exposure.

-

30% Satellite (Local): Invested in high-growth local opportunities, real estate, or local businesses that you can monitor personally.

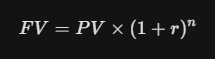

Using the Future Value Formula

If you want to see how your $1,000 today will grow over 20 years in a US index fund versus a local bank, use the Future Value formula:

Where:

-

PV = Your initial $1,000.

-

r = Annualized return (historically ~10% for US stocks).

-

n = Number of years (20).

When you run this math, the compounding power of the US market usually dwarfs local savings accounts, even after accounting for currency exchange fees.

The Final Verdict on US Investing for EM Residents

The truth is that it has never been riskier to stay 100% local. In a world of globalized inflation and digital disruption, the US stock market acts as an essential “firewall” for your wealth.

By investing in US stocks from an emerging market, you are gaining:

-

Access to world-changing innovation.

-

Protection against local currency devaluation.

-

The stability of a world-class legal and regulatory system.

While you must be mindful of taxes and choose the right brokerage, the long-term benefits of a “Dollar-denominated” portfolio are undeniable. Don’t let your geography limit your financial potential.