Where Should You Put Your First $1,000?

Reaching your first $1,000 in savings is a monumental milestone. In a world where 60% of people live paycheck to paycheck, having an extra grand in the bank places you in a position of power. However, that power comes with a critical question: What is the best way to invest it?

The decision you make with this first “seed” will set the tone for your entire financial future. If you put it in the right place, it becomes a wealth-generating engine. If you put it in the wrong place, it might vanish before you even realize its potential.

In this comprehensive guide, we will break down the absolute best strategies for your first $1,000, focusing on risk management, tax efficiency, and long-term growth.

The Pre-Investment Checklist: Don’t Build on Sand

Before we talk about the stock market or crypto, we have to look at your foundation. Investing while your financial “house” is on fire is a recipe for disaster.

Eliminate High-Interest Debt (The Guaranteed Return)

If you have credit card debt, your interest rate is likely between 20% and 30%. There is no investment in the world—not even the best stocks or real estate—that can consistently beat a 25% interest rate.

By paying off $1,000 of credit card debt, you are effectively “earning” a guaranteed 25% return. Before you buy a single share of any company, kill your high-interest debt. It is the single most profitable move you can make.

Build a “Starter” Emergency Fund

Life happens. Tires blow out, medical bills arrive, and laptops break. If you invest your only $1,000 in the stock market and an emergency happens when the market is down, you will be forced to sell at a loss.

Keeping your first $1,000 in a High-Yield Savings Account (HYSA) as a starter emergency fund is a valid “investment.” It buys you the most valuable asset of all: Peace of Mind.

Capture the “Free Money”: The Power of the 401(k) Match

If you are employed and your company offers a 401(k) or similar retirement plan with a “match,” this is the undisputed king of investments.

How the Match Works

If your employer matches 100% of your contributions up to 3% of your salary, and you put in your $1,000, your employer puts in another $1,000. You have instantly achieved a 100% return on investment (ROI).

No professional hedge fund manager can guarantee a 100% return in a day. If you aren’t capturing your employer match, you are essentially leaving part of your salary on the table.

High-Yield Savings Accounts (HYSA): The Safest Bet for Beginners

If you are debt-free and have your employer match covered, the next logical place for $1,000 is a High-Yield Savings Account.

Why an HYSA?

Unlike traditional savings accounts that pay a measly 0.01%, HYSAs (often from online-only banks like Ally, Marcus, or SoFi) can pay upwards of 4.0% to 5.0% interest.

The Math of Inflation

Money sitting in a regular checking account is losing value every day due to inflation. By putting your $1,000 in an HYSA, you are at least protecting your purchasing power while keeping the money liquid (accessible whenever you need it).

The Roth IRA: The Secret Weapon for Tax-Free Wealth

For those looking at the long term, the Roth IRA is arguably the greatest wealth-building tool available to the individual investor.

The Beauty of Tax-Free Growth

In a standard brokerage account, you pay taxes on your gains. In a Roth IRA, you contribute “after-tax” money, but the money grows tax-free, and you can withdraw it tax-free in retirement.

Flexibility for Beginners

A unique feature of the Roth IRA is that you can withdraw your contributions (the original $1,000) at any time without penalty or taxes. While we don’t recommend this, it provides a “safety valve” that other retirement accounts don’t have.

Low-Cost Index Funds: Owning the Entire Market

If you want to put your $1,000 into the stock market but don’t want the stress of picking individual stocks like Apple or Tesla, Index Funds or ETFs are the answer.

The S&P 500 Strategy

An S&P 500 Index Fund (like VOO or SPY) allows you to own a tiny piece of the 500 largest, most successful companies in the United States.

Why Indexing Beats Stock Picking

History shows that 90% of professional investors fail to beat the S&P 500 over a 15-year period. By buying an index fund, you are virtually guaranteed to outperform most “experts.” You aren’t betting on one company; you are betting on the entire economy.

The Mathematics of Starting Early: Compound Interest Explained

Why is the first $1,000 so important? Because of the time value of money. The earlier you start, the less work your money has to do.

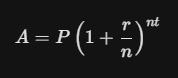

The formula for compound interest is:

Where:

-

A = the final amount.

-

P = the principal ($1,000).

-

r = annual interest rate (e.g., 0.08 for 8%).

-

n = number of times interest is compounded per year.

-

t = number of years.

If you invest $1,000 at age 20 and it grows at an average of 8% annually, by age 65, that single $1,000 will have grown to roughly $32,000 without you ever adding another penny. If you wait until age 30 to invest it, it only grows to about $15,000.

That 10-year delay cost you $17,000.

Investing in Yourself: The “Human Capital” Approach

Sometimes the best place for $1,000 isn’t a bank or a stock. It’s you.

Increasing Your Earning Power

If spending $1,000 on a certification, a coding bootcamp, or a professional course helps you land a job that pays $5,000 more per year, that is a 500% annual return.

In the early stages of your career, your ability to earn more income is your greatest asset. $1,000 invested in your skills can often yield a higher “dividend” than any stock ever could.

Fractional Shares: Diversifying with a Small Budget

In the past, you couldn’t buy a stock if you didn’t have enough to buy one full share. Today, most modern brokerages offer Fractional Shares.

With your $1,000, you can own $100 of ten different “Blue Chip” companies. This allows you to build a diversified “mini-portfolio” that mirrors the big players, even if you are just starting out.

Common Mistakes to Avoid with Your First $1,000

When people get their first grand, they often fall into “get-rich-quick” traps. Stay away from these:

-

Penny Stocks: These are highly volatile and often manipulated. You are more likely to lose 99% than to make 100%.

-

Options Trading: Without proper education, options are a form of gambling that can wipe out your $1,000 in minutes.

-

The “Lambo” Influencers: Anyone promising you a 1,000% return on a “secret” crypto coin is likely selling you a scam.

-

Buying “Things” to Look Rich: A $1,000 watch with $0 in the bank is a sign of poor financial health. A $20 watch with $1,000 in an index fund is the start of a legacy.

Summary: The $1,000 Roadmap

If you are still unsure, follow this simple hierarchy:

-

High-interest debt? Pay it off.

-

No emergency fund? Put it in a High-Yield Savings Account.

-

Employer match available? Max it out.

-

None of the above? Open a Roth IRA and buy a Total Stock Market ETF.

The “truth” about getting rich is that it’s boring. It’s not about one lucky trade; it’s about the habit of investing. Reaching $1,000 is the hard part—you’ve proven you can save. Now, let the math do the rest.