Learn how to build good financial habits in your 20s

Your 20s are often described as the best years of your life. Between finishing education, starting a career, and navigating newfound independence, it is a decade of immense transition. However, from a financial perspective, your 20s are more than just a transition—they are the foundational decade.

The habits you cultivate today will determine whether you spend your 30s and 40s playing “catch-up” or if you spend them watching your wealth grow exponentially. In the world of finance, time is the most valuable commodity, and in your 20s, you have it in abundance. This guide will walk you through the essential strategies to master your money, avoid common pitfalls, and set yourself on the path to true financial independence.

Master the Psychology of Wealth: Habits Over Income

Most people believe that wealth is the result of a high salary. While a high income certainly helps, wealth is actually the result of consistent habits. You likely know someone who earns six figures but lives paycheck to paycheck, and someone with a modest salary who has a robust savings account. The difference is their financial habit loop.

Avoid the “Lifestyle Creep” Trap

As you move from a “broke student” budget to a professional salary, the temptation to upgrade everything is overwhelming. A better car, a nicer apartment, and premium subscriptions seem like a “reward” for your hard work. This is known as lifestyle inflation.

To build wealth, you must maintain a “gap” between what you earn and what you spend. If your income increases by $500 a month, try to save $400 of it. By keeping your expenses low while your income rises, you create a massive engine for wealth creation.

Best Financial Mindset for Young Professionals

Focusing on the “why” before the “how” is crucial. Wealth isn’t about buying things; it’s about buying freedom. When you have a financial cushion, you have the power to leave a job you hate, start a business, or travel without anxiety.

Implement a High-Performance Budgeting System

You cannot manage what you do not measure. In your 20s, you need a system that tracks your cash flow without being so restrictive that you give up after a month.

The 50/30/20 Rule Explained

This is the most effective “layman’s” framework for managing a paycheck:

-

50% for Needs: Rent, groceries, utilities, and transport.

-

30% for Wants: Dining out, hobbies, and entertainment.

-

20% for Financial Goals: This is the most important category. It includes debt repayment, emergency funds, and retirement investments.

Automate Your Finances

The secret to successful budgeting is removing human willpower from the equation. Set up your bank account to automatically transfer your “20% Financial Goals” portion into your savings or investment accounts the moment your paycheck hits. If the money is gone before you see it, you won’t miss it.

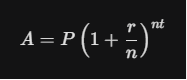

The Math of Millions: Understand the Power of Compound Interest

In your 20s, you have a “superpower” that a 40-year-old cannot buy: Time. Thanks to compound interest, the dollars you save at 22 are significantly more powerful than the dollars you save at 42.

The Cost of Waiting

Consider two investors, Alex and Sam:

-

Alex starts at age 22, investing $300 a month for 10 years, then stops entirely at age 32.

-

Sam waits until age 32 and invests $300 a month every single month until age 62 (30 years).

Despite Sam investing for three times as long, Alex will likely end up with more money at retirement because those early dollars had an extra decade to compound.

Calculating Your Growth

The formula for compound interest shows how your principal (P) grows over time (t) with an interest rate (r):

When t (time) is a large number (like 40 years of a working career), the final amount (A) becomes staggering. Starting today—even with $50—is better than starting next year with $500.

Build an Unshakeable Emergency Fund

Life in your 20s is unpredictable. Jobs change, apartments leak, and cars break down. Without a safety net, these minor inconveniences turn into high-interest credit card debt.

Phase 1: The “Starter” Fund

Your first goal is to save $1,000 to $2,000 as fast as possible. This is your “shield” against the chaos of life. This money should be kept in a separate High-Yield Savings Account (HYSA) so it isn’t tempted by your daily spending.

Phase 2: The 3-6 Month Buffer

Once your high-interest debt is under control, expand that fund to cover 3 to 6 months of your essential living expenses. This provides “FF money”—the ability to walk away from a toxic situation or survive an unexpected layoff without panic.

Crush High-Interest Debt Before It Crushes You

Not all debt is created equal. In your 20s, you likely have a mix of student loans and perhaps some credit card debt. You must prioritize them strategically.

The Credit Card Emergency

If you have credit card debt with an interest rate of 20% or higher, you are in a financial emergency. No investment will consistently return 20%. Therefore, paying off your credit card is the best “investment” you can make. It is a guaranteed return on your money.

Student Loan Strategy

For student loans with lower interest rates (under 5%), it may be better to pay the minimum and invest your extra cash in the stock market, where historical returns average 7–10%. However, the psychological relief of being debt-free is also a valid reason to pay them off early.

Master Your Credit Score Early

Your credit score is your “financial GPA.” In your 20s, you are building the history that will determine the interest rate on your future mortgage or car loan. A poor score can cost you hundreds of thousands of dollars in extra interest over your lifetime.

How to Build a Perfect Score

-

Pay Everything on Time: One late payment can tank your score by 100 points. Use autopay for at least the minimum amount due.

-

Keep Utilization Low: Don’t max out your cards. Try to use less than 10% of your total limit.

-

Length of History: Do not close your oldest credit card accounts. The longer your history, the better you look to lenders.

Investing for Beginners: Harnessing the Stock Market

Many 20-somethings avoid the stock market because it feels like “gambling.” In reality, the stock market is the most effective wealth-building machine in history—if you use it correctly.

Retirement Accounts: 401(k) and Roth IRA

-

The 401(k) Match: If your employer offers a 401(k) match, that is a 100% return on your money. It is a part of your salary that you only receive if you contribute. Always take the full match.

-

The Roth IRA: This is a 20-something’s best friend. You pay taxes on the money now (when your tax bracket is likely low), and the money grows and is withdrawn 100% tax-free in retirement.

Index Funds: The “Set and Forget” Method

You don’t need to be a stock market genius. By buying a Low-Cost S&P 500 Index Fund, you own a small piece of the 500 largest companies in America. You aren’t betting on one company; you are betting on the growth of the entire economy.

Negotiate Your Salary: Your Career is Your Largest Asset

In your 20s, your greatest financial asset isn’t your bank account—it’s your earning potential. A $5,000 increase in your starting salary, when compounded over a 40-year career with raises, can result in over $1,000,000 in additional lifetime earnings.

How to Negotiate

-

Research: Use sites like Glassdoor or Payscale to know the market rate for your role.

-

Quantify Your Value: Instead of saying “I work hard,” say “I increased efficiency by 15% or managed a budget of $50k.”

-

Be Prepared to Walk: The best negotiation position is being okay with the current status quo while knowing your worth elsewhere.

Navigate Big Purchases with Wisdom

Your 20s are full of pressure to “look” successful. This often leads to two major financial mistakes: expensive cars and premature home buying.

The Car Trap

A car is a depreciating asset. The moment you drive it off the lot, it loses value. Many young professionals trap themselves in $600/month car payments that prevent them from investing. Aim to buy a reliable, used vehicle and drive it until the wheels fall off.

Renting is Not “Throwing Money Away”

In your 20s, renting provides mobility. If a better job opportunity appears in another city, you can move at the end of your lease. Buying a home involves high closing costs and maintenance risks. Only buy a home when you are certain you will stay for 5–7 years and your finances are rock solid.

Protect Yourself: The Role of Insurance

One medical emergency or a lawsuit can wipe out years of hard work. Part of good financial habits is “defensive” planning.

-

Health Insurance: This is non-negotiable. Even a “catastrophic” plan is better than no plan.

-

Renters Insurance: For about $15 a month, it protects your belongings from fire, theft, or water damage.

-

Disability Insurance: You are more likely to become disabled during your working years than you are to die. This insurance protects your ability to earn an income.

The “Invisible” Habits: Taxes and Side Hustles

Tax Literacy

Understand the difference between a deduction and a credit. Use accounts like an HSA (Health Savings Account) if you have a high-deductible health plan. An HSA is “triple-tax advantaged”: money goes in tax-free, grows tax-free, and comes out tax-free for medical expenses.

The Side Hustle Balance

While side hustles are a great way to boost income in your 20s, ensure they don’t lead to burnout or distract you from your primary career growth. Use side hustle money exclusively for “Financial Goals” (investing/debt) rather than lifestyle upgrades.

Your Future Self is Watching

Building good financial habits in your 20s isn’t about depriving yourself of joy. It’s about intentionality. It’s about deciding that you want to be a person who controls their money rather than a person whose money controls them.

If you start today—by tracking your spending, opening a Roth IRA, and avoiding high-interest debt—you are making a promise to your future self. You are giving yourself the gift of options, security, and wealth. Financial freedom isn’t a destination you reach in your 60s; it’s a habit you start right now.

Take Action This Week:

-

Check your Credit Score: Use a free tool to see where you stand.

-

Open a HYSA: Move your emergency savings to an account that pays at least 4% interest.

-

Audit your Subscriptions: Cancel three things you haven’t used in the last month.

-

Invest $50: Open a brokerage account and buy a total market index fund just to get over the “starting” hurdle.

The best time to plant a tree was 20 years ago. The second best time is today. Start growing your financial forest now.