How Much of Your Portfolio Should Be in Crypto?

The conversation surrounding cryptocurrency has undergone a radical transformation over the last decade. In the early 2010s, Bitcoin was a niche experiment. By the early 2020s, it was a speculative frenzy. Now, in 2026, cryptocurrency has matured into a recognized asset class, sitting alongside stocks, bonds, and real estate in the portfolios of both retail investors and institutional giants.

However, the million-dollar question remains: How much is too much?

Determining the “perfect” percentage for your crypto allocation isn’t just about picking a number out of a hat. It involves a deep dive into risk tolerance, time horizons, and the mathematical principles of Modern Portfolio Theory. This guide will help you navigate these waters to find an allocation that maximizes your growth without compromising your financial security.

The Evolution of Crypto in Modern Portfolio Theory (MPT)

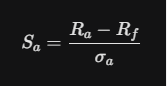

To understand how much crypto you should own, we first have to understand why we own it at all. Historically, the goal of an investment portfolio was to achieve the highest possible return for the lowest possible risk. This is often measured by the Sharpe Ratio.

In this formula, Ra is the asset return, Rf is the risk-free rate, and Aa is the standard deviation (volatility).

For years, critics argued that crypto’s volatility (Aa) was too high to justify its place in a balanced portfolio. However, backtesting has shown that even a tiny allocation (1% to 5%) to Bitcoin historically increased a portfolio’s total return significantly while only marginally increasing the overall risk profile. This is due to low correlation—the tendency of crypto to move independently of the S&P 500 or the bond market (though this correlation has tightened in recent years).

The Conservative Approach: The “1% to 5%” Rule

For most financial advisors and traditional investors, the “sweet spot” for cryptocurrency remains in the single digits. This is often referred to as a “non-zero” allocation.

Why 1% to 5%?

The logic here is simple: Asymmetric Risk.

If you invest 1% of your wealth in crypto and it goes to zero, your lifestyle doesn’t change. You might miss a nice vacation, but your retirement remains intact. However, if that 1% performs a 10x or 100x move—as Bitcoin and Ethereum have done in the past—it can add a significant “boost” to your total net worth.

-

Who it’s for: Investors nearing retirement, those with low risk tolerance, or those who already have significant exposure to high-growth tech stocks.

-

The Goal: Wealth preservation with a small “kicker” for growth.

The Moderate Approach: The “5% to 15%” Allocation

In 2026, a 10% crypto allocation is no longer considered “reckless” by many mainstream standards. With the maturity of Bitcoin and Ethereum Spot ETFs (Exchange Traded Funds), the “plumbing” of the crypto market is much safer than it was in the era of unregulated exchanges.

The Balanced Multi-Asset Strategy

A moderate investor might look at their portfolio as a 60/30/10 split:

-

60% Stocks/Equities (Index funds, ETFs).

-

30% Fixed Income/Bonds (Stability and yield).

-

10% Digital Assets (High-growth potential).

At this level, you are no longer just “dipping your toe in the water.” You are actively betting on the long-term adoption of blockchain technology. At 10%, a market crash in crypto (e.g., a 50% drop) would result in a 5% total portfolio drawdown. For most disciplined investors, this is manageable.

The Aggressive Approach: 20% and Beyond

High-conviction investors, particularly those in younger demographics with decades of earning potential ahead of them, often push their crypto allocation into the 20% to 30% range.

The “Wealth Accelerator” Mentality

If you are in your 20s or 30s, your greatest asset is Time. You can afford to endure a multi-year “Crypto Winter” because you don’t need to liquidate your assets for decades. At this allocation level, you aren’t just looking for a “boost”; you are looking to accelerate your path to financial independence.

Warning: Going above 20% requires a high degree of “stomach.” You must be prepared to see your total net worth fluctuate by 5% to 10% in a single week without panic-selling.

Factors That Should Dictate Your Crypto Allocation

There is no “one size fits all” number. Your specific percentage should be filtered through these four critical lenses:

1. Age and Time Horizon

The closer you are to needing your money, the less crypto you should own. If you are 65 and retiring next year, a 20% crypto crash could permanently impair your ability to pay bills. If you are 25, that same crash is merely a “buying opportunity.”

2. Debt-to-Income Ratio

Do you have high-interest credit card debt or a massive mortgage? If so, your “crypto allocation” should probably be 0% until your high-interest debt is cleared. Investing in a volatile asset while paying 20% interest on a credit card is mathematically illogical.

3. Emergency Fund Status

Before allocating to crypto, you should have 3 to 6 months of living expenses in a “boring” high-yield savings account. Crypto is not an emergency fund. You do not want to be forced to sell your Bitcoin at the bottom of a market cycle because your car broke down.

4. Psychological Resilience

Be honest with yourself. How did you feel the last time the stock market dropped 2%? If that made you anxious, crypto’s 20% swings will be unbearable. Your allocation should never exceed your “Sleep Point”—the amount you can own without losing sleep over the price.

Diversification Within the Crypto Sleeve

Once you’ve decided that, for example, 10% of your total portfolio will be in crypto, you have to decide how to split that 10%. Not all digital assets carry the same risk.

The Blue-Chip Foundation (Bitcoin & Ethereum)

For most, at least 70% of the crypto “sleeve” should be in Bitcoin (BTC) and Ethereum (ETH). These are the “Blue Chips” of the space. They have the highest liquidity, institutional backing, and the most established regulatory status.

The Mid-Cap Growth (Altcoins)

The remaining 20-30% can be allocated to “Altcoins”—projects like Solana, Layer 2 scaling solutions, or decentralized finance (DeFi) protocols. These have higher upside potential than Bitcoin but come with a significantly higher risk of going to zero.

Stablecoins for Yield

In 2026, many investors use a portion of their crypto allocation for Stablecoin Lending. By holding assets pegged to the US Dollar (like USDC) and lending them out through regulated platforms, you can often earn yields that outperform traditional savings accounts without the price volatility of Bitcoin.

The Importance of Rebalancing: Don’t Let Crypto Take Over

One of the biggest mistakes investors make is failing to rebalance.

Imagine you start with a 5% crypto allocation. In a massive bull market, your crypto doubles while your stocks stay flat. Suddenly, crypto makes up 10% of your portfolio. You are now twice as “risky” as you intended to be.

How to Rebalance Effectively:

-

Time-Based: Every six months, sell some of your crypto gains to buy more stocks/bonds (or vice-versa) to return to your target percentage.

-

Threshold-Based: If your allocation moves more than 25% away from your target (e.g., your 10% target becomes 12.5%), trigger a rebalance.

This forces you to “Buy Low and Sell High”—the holy grail of investing. You are essentially harvesting profits from your “winners” and moving them into “undervalued” assets.

Tax Implications of Your Crypto Allocation

In the United States and many other jurisdictions, crypto is taxed as property. Every time you rebalance (sell crypto for a profit), you trigger a Capital Gains Tax.

If you are a high-net-worth investor, you might consider holding your crypto allocation within a Self-Directed IRA. This allows your crypto to grow tax-free (in a Roth) or tax-deferred (in a Traditional IRA), which can save you hundreds of thousands of dollars in the long run.

Finding Your Personal “Golden Ratio”

So, how much of your portfolio should be in crypto?

For the vast majority of people, the answer is somewhere between 1% and 10%. This range provides enough exposure to catch the “upside” of the digital revolution without risking total financial ruin during the inevitable “downside” cycles.

Wealth is built through consistency and discipline, not through “betting the farm” on a single asset. Start with an amount that feels like a “learning experiment,” observe your emotional reaction to the volatility, and slowly scale up as your knowledge and confidence grow.

Remember: The goal isn’t just to be “crypto-rich”—it’s to be financially free. A balanced, diversified portfolio is the surest path to that destination.

Quick Summary Checklist:

-

Conservative: 1% – 3% (Low risk, “FOMO” insurance).

-

Moderate: 5% – 10% (Growth-focused, balanced).

-

Aggressive: 15% – 25% (High conviction, young investors).

-

Debt Check: Pay off high-interest debt before buying crypto.

-

Rebalance: Check your percentages every 6 months.

Is your current portfolio ready for the digital age, or are you still playing by the old rules?