How to Build Passive Income with $500 a Month

The dream of “making money while you sleep” is often dismissed as a fantasy reserved for tech moguls or lottery winners. However, as we navigate the financial landscape of 2026, the barriers to entry for creating recurring revenue have never been lower. You don’t need a million dollars to start; you need a strategy, a bit of discipline, and a consistent contribution.

Building a significant stream of passive income with $500 a month is not just possible—it is a mathematically proven path to financial independence. In this comprehensive guide, we will break down the strategies, the math, and the mindset required to turn a modest monthly investment into a life-changing income engine.

The Philosophy of Passive Income: Understanding the “Front-Loaded” Effort

Before we dive into the “where” and “how,” we must address the “what.” Passive income is often misunderstood as “free money.” In reality, passive income is delayed gratification. You are putting in a massive amount of effort (or capital) upfront so that you can reap the rewards later.

There are three main “currencies” you can use to build passive income:

-

Money (Capital): Investing your cash into assets that pay you back.

-

Time: Spending hours building a digital product or business.

-

Labor: Doing the work once to create a recurring value.

When you invest $500 a month, you are using Capital to buy back your future time. The goal is to reach a “crossover point” where the income generated by your investments exceeds your monthly living expenses.

Why $500 a Month is the “Sweet Spot” for Modern Investors

You might think $500 isn’t enough to make a difference. But in the world of compounding, $500 is a powerful engine.

The Mathematics of a $500 Monthly Contribution

If you invest $500 every month and achieve an average annual return of 8% (the historical average of the stock market adjusted for inflation), here is what your “passive income engine” looks like over time:

-

Year 10: You’ve invested $60,000, but your account is worth roughly $91,473.

-

Year 20: Your account has grown to approximately $294,510.

-

Year 30: You are sitting on nearly $745,179.

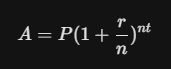

The compound interest formula demonstrates this growth:

At a 4% withdrawal rate (a standard rule of thumb in retirement planning), a $745,000 portfolio would provide you with $29,800 a year—roughly $2,483 a month—in completely passive income. This is the power of starting small and staying consistent.

Strategy 1: Dividend Growth Investing for Consistent Cash Flow

One of the most reliable ways to build passive income with $500 a month is through Dividend Growth Investing. When you buy shares of a dividend-paying company, you are essentially becoming a part-owner of a business that sends you a check every quarter just for holding their stock.

Identifying Dividend Aristocrats and Kings

For beginners, the safest bet is to look at “Dividend Aristocrats”—companies in the S&P 500 that have not only paid but increased their dividend payments for at least 25 consecutive years. These are stable, blue-chip giants like Johnson & Johnson, Procter & Gamble, or PepsiCo.

The Power of the DRIP (Dividend Reinvestment Plan)

The secret to maximizing this strategy is the DRIP. Instead of taking the cash dividends and spending them, you instruct your brokerage to automatically use that money to buy more shares of the stock. This creates a “snowball effect” where you own more shares, which pay more dividends, which buy even more shares.

In 2026, most major US brokerages offer “fractional shares,” meaning your $500 can be spread across 20 or 30 different dividend-paying companies effortlessly.

Strategy 2: Utilizing REITs for Real Estate Exposure

Real estate is a classic passive income play, but most people don’t have the down payment for a physical property. This is where REITs (Real Estate Investment Trusts) come in.

How REITs Work

A REIT is a company that owns, operates, or finances income-producing real estate. By law, REITs must distribute at least 90% of their taxable income to shareholders in the form of dividends.

Why REITs are Perfect for a $500 Budget

You can buy shares of a REIT just like a stock. With $500, you can own a piece of a data center, a hospital network, or a massive apartment complex. You get the monthly or quarterly “rental” income without ever having to fix a leaky faucet or chase down a tenant for rent.

Strategy 3: Low-Cost Index Funds and ETFs (The “Set and Forget” Method)

If picking individual stocks feels too risky or time-consuming, Exchange-Traded Funds (ETFs) are your best friend. An ETF allows you to buy a “basket” of hundreds of stocks in a single transaction.

Top ETFs for Passive Income in 2026

-

SCHD (Schwab US Dividend Equity ETF): Focuses on high-quality companies with sustainable dividends.

-

VYM (Vanguard High Dividend Yield ETF): Provides exposure to companies with higher-than-average yields.

-

VTI (Vanguard Total Stock Market ETF): Captures the growth of the entire US economy.

By putting your $500 a month into a diversified ETF, you are betting on the collective ingenuity of the world’s best companies. It requires zero maintenance and offers excellent long-term security.

Strategy 4: High-Yield Savings and CDs in a 2026 Interest Environment

In 2026, interest rates have stabilized at a level where “cash” actually pays. While not a way to get rich quickly, High-Yield Savings Accounts (HYSA) and Certificates of Deposit (CDs) are vital for the “safe” portion of your passive income strategy.

The “Cash Cushion” Strategy

Before going all-in on stocks, use your first few months of $500 payments to build a high-yield emergency fund. With rates sitting in a healthy range, your “boring” savings account can generate enough passive interest to cover a small bill every month. This provides the psychological “win” needed to keep the momentum going.

Strategy 5: Digital Assets and the “Content Capital” Method

This is where passive income gets creative. Instead of just buying assets, you can use your $500 a month to fund the creation of digital assets.

Building a Digital Portfolio

-

Content Sites/Blogs: Use your $500 to pay for high-quality hosting, SEO tools, and perhaps a freelance writer or an AI-content editor. Over 12–24 months, a well-optimized site can generate thousands in monthly ad revenue and affiliate commissions.

-

Online Courses: Use the money to buy professional recording gear or AI video tools. Once the course is hosted on a platform like Udemy or Teachable, it sells itself while you sleep.

-

Digital Templates: Whether it’s Notion templates or Excel budget sheets, the cost to create them is your time, and the $500 can be used for marketing and ads to drive sales.

The goal here is to use your capital to “buy” the tools required to create an asset that has zero marginal cost of reproduction.

Strategy 6: Peer-to-Peer (P2P) Lending and Private Credit

In 2026, the world of “Private Credit” has become more accessible to the average investor. Through P2P platforms, you can lend your $500 directly to individuals or small businesses in exchange for interest payments.

Understanding the Risk/Reward

Because you are “acting as the bank,” you can often earn interest rates significantly higher than what a savings account offers. However, this comes with the risk of default. The key is to diversify—instead of lending $500 to one person, lend $25 to 20 different people.

Tax Optimization: Why Where You Invest Matters

If you want to maximize your passive income, you have to minimize what you give to the government. In the US, utilizing tax-advantaged accounts is non-negotiable.

The Roth IRA: The Holy Grail

If you invest your $500 a month into a Roth IRA, your money grows tax-free, and your withdrawals in retirement are completely tax-free. This means the government doesn’t take a cut of your dividends or your capital gains.

The Taxable Brokerage Account

If you need access to your passive income before retirement age, you’ll use a standard brokerage account. While you’ll pay taxes on your dividends (usually at the “Qualified Dividend” rate, which is lower than ordinary income), this provides the flexibility to retire early.

Common Pitfalls to Avoid When Building Passive Income

Many people start their journey with $500 a month but quit after six months. Here is why they fail:

-

Chasing “Yield Traps”: Don’t buy a stock just because it pays a 15% dividend. Often, a yield that high is a sign that the company is in trouble and about to cut its payment.

-

Lack of Patience: Passive income is a marathon. The first few years will feel like you are moving in slow motion. Do not check your balance every day.

-

High Fees: Be wary of financial advisors who want to charge you a 1% management fee. On a small portfolio, fees can eat up nearly half of your potential gains over 30 years. Stick to low-cost index funds.

The Best Time to Start was Yesterday

Building passive income with $500 a month isn’t about being a math genius; it’s about being a consistent investor. The 2026 economy offers more tools, more access, and more data than ever before.

The difference between the person who retires with a $2,000 monthly passive income and the person who retires with nothing isn’t their salary—it’s their habit. Start your $500 monthly transfer today. Your future self is waiting to thank you.