Understand the difference between saving and investing

In the world of personal finance, words like “saving” and “investing” are often tossed around as if they mean the same thing. You might hear a friend say they are “saving for retirement in the stock market,” or a relative mention they are “investing in a high-yield savings account.” While both are essential habits for anyone looking to build a stable future, they are fundamentally different tools with very different purposes.

Think of it this way: Saving is like gathering nuts for the winter; investing is like planting a nut tree that will feed you for decades.

If you want to master your money in 2026, you need to understand exactly when to use each strategy. In this deep-dive guide, we will break down the mechanics of saving and investing, explore the psychological barriers to both, and help you determine the perfect balance for your unique life stage.

Defining Saving: The Essential Safety Net for Your Daily Life

At its core, saving is the act of setting aside money in a safe, liquid environment where it is easily accessible. When you save, your primary goal is not necessarily to “make money” on your money, but to ensure that the principal—the original amount you put in—remains intact and available whenever you need it.

The Pillars of a Solid Saving Strategy

-

Liquidity: This is the most important feature of saving. If your car breaks down or you have a medical emergency, you need cash now. Saving accounts, money market accounts, and short-term CDs (Certificates of Deposit) offer high liquidity.

-

Safety: Saving is low-risk. In most modern banking systems, your savings are insured up to a certain amount. You don’t have to worry about waking up to find that half of your emergency fund has vanished due to a market crash.

-

Specific Goals: Saving is usually geared toward short-term needs—anything from an emergency fund (3 to 6 months of expenses) to a down payment for a house or a vacation fund.

Why Every Investor Must Be a Saver First

You cannot build a skyscraper on a swamp. Similarly, you cannot build an investment portfolio on a shaky financial foundation. Before you buy your first stock or fractional share of real estate, you must have a “Savings Buffer.” Without it, the first minor crisis will force you to sell your investments at a loss just to cover your bills.

Defining Investing: The Growth Engine for Long-Term Wealth

If saving is about preservation, investing is about multiplication. Investing is the process of using your money to buy assets that you believe will increase in value over time or generate an income stream.

The Mechanics of Asset Appreciation

When you invest, you are typically buying a piece of something—a company (stocks), a loan (bonds), or property (real estate). You are accepting a certain level of risk in exchange for the potential of a higher return.

Unlike a savings account, where you might earn a tiny bit of interest, an investment can grow significantly. However, it can also lose value. This is the trade-off: you give up the absolute safety of cash for the opportunity to outpace inflation and build real wealth.

The Power of “Ownership”

Investors are owners. When you own shares in a company, you are participating in that company’s success. As the world economy grows, the companies within it grow, and as an investor, your net worth grows alongside them. This is how the “wealthy get wealthier”—they move their money out of stagnant cash and into productive assets.

Risk vs. Reward: Understanding the Fundamental Trade-off

One of the hardest concepts for beginners to grasp is that having “no risk” is actually a risk in itself. ### The Illusion of Safety in Cash

Many people feel “safe” when they see a large balance in their traditional savings account. However, if that account is only paying 0.01% interest while the cost of bread, milk, and rent is rising by 3% or 4% per year, that person is actually losing purchasing power. Investing introduces market risk (the price could go down), but it protects you against inflation risk (the risk that your money will buy less in the future).

Calculating Your Risk Tolerance

Your “profile” as a saver or investor depends on your risk tolerance, which is influenced by:

-

Time Horizon: How soon do you need the money? (If it’s in 20 years, you can handle more risk).

-

Emotional Temperament: Can you stay calm if your portfolio drops 10% in a month?

-

Financial Stability: Do you have a stable job and a full emergency fund?

The Hidden Thief: How Inflation Erodes Your Stagnant Savings

To understand why you can’t just “save” your way to retirement, you have to understand inflation. Inflation is the rate at which the general level of prices for goods and services is rising.

A Real-World Example

Imagine you have $10,000 under your mattress. If inflation is at 3%, in 10 years, that $10,000 will only buy what $7,440 buys today. You haven’t “lost” any dollar bills, but the value of those bills has evaporated.

Investing as an Inflation Shield

Historically, the stock market and real estate have outpaced inflation over long periods. By investing, you are essentially trying to make sure your money grows faster than the cost of living. If inflation is 3% and your investments grow by 7%, you have a “real” return of 4%. This is how you actually get ahead.

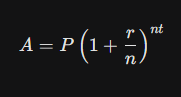

Compound Interest: The Eighth Wonder of the World

The most powerful argument for investing over saving is the phenomenon of Compound Interest. This is when the interest you earn on your money begins to earn interest on itself.

The Mathematical Formula

In financial modeling, the formula for compound interest is:

Where:

-

A = the future value of the investment/loan, including interest

-

P = the principal investment amount (the initial deposit)

-

r = the annual interest rate (decimal)

-

n = the number of times that interest is compounded per unit t

-

t = the time the money is invested or borrowed for

The Snowball Effect

Imagine you start with $1,000 and it grows by 10% this year. You now have $1,100. Next year, that 10% isn’t calculated on your original $1,000; it’s calculated on $1,100. You earn $110 instead of $100.

Over 30 or 40 years, this effect becomes astronomical. A small amount of money invested early in life can grow to be much larger than a huge amount of money saved late in life. Time is the most important variable in the equation, which is why starting to invest—even with small amounts—is so critical.

Time Horizons: When to Choose One Over the Other

A simple rule of thumb in 2026 is to look at your “Time Horizon.” This is the length of time you expect to hold an investment before you need the money back.

Short-Term Goals (0–3 Years) -> SAVE

If you are planning to buy a car next year or pay for a wedding in 18 months, do not invest that money. The stock market is too volatile in the short term. You don’t want to find out a month before your wedding that the market is down 20% and you can no longer afford the venue. Keep this money in a High-Yield Savings Account (HYSA).

Mid-Term Goals (3–7 Years) -> A HYBRID APPROACH

For goals like buying a house in five years, you might use a mix of safe savings and conservative investments (like bonds or balanced ETFs). This allows for some growth while protecting most of the principal.

Long-Term Goals (7+ Years) -> INVEST

For retirement, your child’s college fund, or building generational wealth, investing is the clear winner. Over periods of a decade or more, the probability of the market being higher than when you started is very high, and the benefits of compound interest are most pronounced.

The Bridge: Building Your Emergency Fund Before You Start

We’ve established that investing is better for growth, but you cannot skip the “Saving” phase. The bridge between the two is the Emergency Fund.

How Much Is Enough?

Most experts recommend saving 3 to 6 months of essential living expenses. This includes rent/mortgage, utilities, groceries, and insurance.

-

Save 3 months if you have a very stable job and low debt.

-

Save 6+ months if you are self-employed, work in a volatile industry (like tech or entertainment), or have dependents.

Where to Keep It

This money should be kept separate from your daily checking account so you aren’t tempted to spend it on non-emergencies. However, it should be in an account that allows for instant transfers. In 2026, many digital banks offer “vaults” or “buckets” that help you visualize this progress.

Common Investment Vehicles: From Stocks to Shiba Inu

Once you have your savings in order, where do you actually put your investment money? The options can be overwhelming, especially with the rise of digital assets.

The Classics: Stocks and Bonds

-

Stocks (Equities): You buy a “share” of a company. Highest potential for growth, but highest volatility.

-

Bonds (Fixed Income): You are basically acting as the bank and lending money to a government or corporation. Lower risk, lower return.

The Modern Staples: ETFs and Mutual Funds

Instead of picking one stock (like Apple or Tesla), you buy a “basket” of hundreds of stocks. This is called diversification. If one company fails, the other 499 in the fund keep you afloat. For laypeople, S&P 500 Index Funds are often the most recommended starting point.

The “Wild Cards”: Cryptocurrency

As mentioned in our user community discussions, interest in Bitcoin, Ethereum, and even meme coins like Shiba Inu is at an all-time high.

-

The Reality Check: These are highly speculative. While they have seen massive gains, they can also drop 80% in a week. If you choose to invest here, it should only be with money you are 100% prepared to lose, and it should represent a small percentage of your total portfolio.

The Psychology of Money: Fear of Loss vs. Greed for Growth

Why is it so hard for people to switch from saving to investing? It’s not a lack of math skills; it’s our biology.

Loss Aversion

Psychologists have found that the pain of losing $100 is twice as strong as the joy of gaining $100. This is why people stay in “safe” savings accounts even when they know they are losing money to inflation. Our brains are wired to protect what we have, not to hunt for what we could have.

Analysis Paralysis

In 2026, we have too much information. Between TikTok financial gurus, YouTube analysts, and AI-driven news feeds, many people get overwhelmed and do nothing. They wait for the “perfect” time to invest.

-

The Truth: “Time in the market” is more important than “timing the market.” Most of the stock market’s biggest gains happen on just a few days of the year. If you are sitting on the sidelines waiting for a crash, you will likely miss the recovery.

Diversification: Why You Shouldn’t Put All Your Eggs in One Basket

Whether you are saving or investing, the principle of diversification is your best defense against disaster.

Saving Diversification

Don’t keep all your cash in a single physical location or even a single bank if you have very high balances. Ensure your bank is FDIC (or equivalent) insured.

Investment Diversification

This is where the magic happens. A well-diversified portfolio might look like this:

-

60% Domestic Stocks (Broad market index)

-

20% International Stocks

-

10% Bonds (For stability)

-

5% Real Estate (REITs)

-

5% Alternative Assets (Gold, Crypto, or Art)

By spreading your money across different “asset classes,” you ensure that when one sector is struggling, another might be thriving. This smoothes out the “rollercoaster” of investing and makes it much easier to sleep at night.

The Opportunity Cost: What Are You Giving Up?

In finance, Opportunity Cost is the loss of potential gain from other alternatives when one alternative is chosen.

The Cost of Being “Too Safe”

If you keep $50,000 in a savings account for 20 years, you might feel safe. But if that money could have been in an index fund earning 7% annually, the “cost” of your safety is over $140,000 in lost gains.

That is the price of fear. You aren’t just “not making money”; you are actively giving up a much wealthier future version of yourself. This is why understanding the difference between these two paths is so vital for long-term survival in a modern economy.

Creating Your Personal Financial Mix

So, should you save or should you invest? The answer is: Yes.

You need both. You need the “brakes” of a savings account to protect you from life’s unexpected turns, and you need the “engine” of an investment portfolio to drive you toward retirement and financial independence.

Your 3-Step Action Plan for 2026

-

The Starter Save: Get $1,000 to $2,000 into a high-yield savings account immediately. This stops you from using high-interest credit cards when things go wrong.

-

The Bridge: Build that savings up to 3 months of expenses. Once this is done, you have “permission” to be aggressive with your growth.

-

The Automation: Set up an automatic transfer to an investment account. Even $50 a month into a total market ETF will trigger the power of compound interest.

Financial freedom isn’t about being a genius; it’s about being consistent. By respecting the safety of savings and embracing the power of investing, you are setting yourself up for a life where you control your money, rather than your money controlling you.