How to Reprogram Your Mind to Save More Money

Most personal finance advice focuses on the “what”: what to invest in, what budget to use, and what apps to download. But if wealth were simply a matter of information, we would all be millionaires. The reality is that saving money is 20% head knowledge and 80% behavior.

To truly change your financial trajectory, you don’t just need a new spreadsheet; you need to reprogram your mind.

In the modern landscape of 2026, we are bombarded by sophisticated algorithms designed to trigger our impulsive “buy” instincts. To fight back, you must understand the psychological traps that keep you spending and learn how to rewire your brain for long-term abundance. This guide will walk you through the neurobiology of spending and provide actionable psychological hacks to turn you into a natural saver.

Understanding the Evolutionary Gap: Why Your Brain Hates Saving

To fix a problem, you must first understand its source. Human beings are operating with 10,000-year-old biological hardware in a 21st-century digital world.

The Survival Instinct of Scarcity

For our ancestors, “saving” was a death sentence. If they found a high-calorie food source, they had to consume it immediately because it wouldn’t be there tomorrow. This created a biological bias toward Instant Gratification.

In your brain, this is a battle between the Amygdala (the emotional, survival-based center) and the Prefrontal Cortex (the rational, long-term planning center). When you see a “Limited Time Offer,” your Amygdala screams, “Acquire this now for survival!” meanwhile, your Prefrontal Cortex is too slow to remind you about your retirement goals. Reprogramming your mind starts with recognizing that your urge to spend is often just an outdated survival reflex.

Identify and Rewrite Your “Money Scripts”

A “Money Script” is a subconscious belief about money that you developed during childhood. These scripts run in the background like a computer operating system, dictating every financial decision you make.

Common Destructive Money Scripts

-

Money Avoidance: The belief that money is “dirty” or that rich people are greedy.

-

Money Status: The belief that your self-worth is tied to your net worth.

-

Money Worship: The belief that more money will solve every problem.

-

Money Vigilance: Extreme anxiety about saving, leading to a “scarcity mindset” that prevents you from enjoying life.

How to Reprogram the Script

Take a moment to write down what your parents said about money. If the script was “We can’t afford that,” your brain might be stuck in a scarcity loop. Change it to: “We choose to prioritize our wealth over that specific item.” By changing the language from deprivation to agency, you take the power back.

Cognitive Reframing: Saving as “Buying Freedom”

One of the biggest psychological hurdles to saving is that it feels like loss. When you move $500 to a savings account, your brain feels like it just “lost” $500 that it could have used for something fun.

The Power of Reframing

To save more, you must reframe the act of saving. You aren’t “saving” money; you are buying freedom.

-

Instead of seeing a $100 savings deposit as a missed dinner, see it as buying two days of independence in the future.

-

Instead of seeing a used car as a “downgrade,” see it as buying a year of early retirement.

When you shift the focus from what you are giving up to what you are acquiring (time, security, freedom), your brain’s reward system begins to favor the act of saving.

The “Friction” Method: Hacking Your Impulse Spending

In behavioral finance, “friction” is any obstacle that stands between you and an action. If you want to save more, you must decrease friction for saving and increase friction for spending.

How to Increase Spending Friction

-

Delete Saved Credit Cards: Remove your card info from Amazon, food delivery apps, and your browser. Forcing yourself to manually type in those 16 digits gives your Prefrontal Cortex time to “wake up” and veto the purchase.

-

The 48-Hour Rule: For any non-essential purchase over $50, wait 48 hours. The dopamine spike that drives impulse buys usually fades within 24 hours.

-

Unsubscribe: Your inbox is a minefield of marketing. Unsubscribe from retail newsletters to stop the “Sale” notifications from triggering your Amygdala.

How to Decrease Saving Friction

-

Automate Everything: This is the “Lazy Discipline” secret. If the money moves to your high-yield savings account before you ever see it in your checking, you don’t have to use any willpower to save.

Bridging the Empathy Gap with Your “Future Self”

Psychological studies using fMRI scans have found something shocking: when people think about their “Future Self,” their brain reacts as if they are thinking about a complete stranger.

The Empathy Gap

This is why it’s so easy to spend money today at the expense of “Future You.” To your brain, you are essentially giving money to someone you don’t know.

The Mind Hack: Connect with the Stranger

To reprogram this, you need to build empathy for your future self.

-

Visualization: Spend 5 minutes a week visualizing your life in 20 years. What kind of coffee are you drinking? Where are you sitting?

-

Age-Filtering: Use an app to see what you will look like at age 70. Keep that photo near your desk. It sounds silly, but it creates a visceral connection that makes you want to protect that “stranger” from financial hardship.

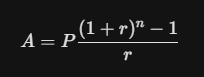

The Mathematics of “Why”: Understanding the Reward

Reprogramming is easier when the brain understands the sheer mathematical power of saving. Most laypeople underestimate the “cost” of small daily habits because they don’t see the Compound Interest math.

The True Cost of a $\$5$ Habit

If you save $\$5$ a day (the price of a latte) and invest it with a $10\%$ annual return, look at what happens over time:

| Timeframe | Total Saved + Interest |

| 10 Years | $30,500 |

| 20 Years | $111,300 |

| 30 Years | $322,000 |

When your mind realizes that a small, insignificant daily “want” is actually a $\$322,000$ opportunity cost, it becomes much easier to resist the impulse.

Combatting “Lifestyle Creep” through Hedonic Adaptation

Hedonic Adaptation is the psychological process where humans quickly return to a stable level of happiness despite major positive or negative changes.

The “New Car” Fallacy

You buy a new car, and for two weeks, you feel amazing. A month later, it’s just “your car.” Your happiness level has returned to baseline, but your $\$600$ monthly payment remains.

How to Hack the Treadmill

To reprogram your mind, you must recognize that “stuff” will not provide a permanent boost to your happiness. Instead, spend your money on Experiences or Time. Research shows that “Buying Time” (e.g., paying for a house cleaner so you can spend time with family) leads to a much higher and more sustained level of happiness than buying a luxury item.

Identifying Your Emotional Triggers

Spending is rarely about the product; it’s about the emotion. Many of us are “Emotional Spenders” who use retail therapy to cope with:

-

Stress: “I had a hard day; I deserve this.”

-

Loneliness: “A new outfit will make me feel seen.”

-

Boredom: Scrolling through shopping apps as a hobby.

The “HALT” Method

Before you buy anything, ask yourself if you are: Hungry, Angry, Lonely, or Tired. If you are any of those four, your rational brain is offline. Close the laptop and address the underlying emotion first. Reprogramming your mind means learning to soothe your emotions with something other than a credit card.

Social Proof and the “Comparison Trap”

We are social animals. In the past, being “different” from the tribe meant being left for dead. Today, we use Conspicuous Consumption to prove we belong.

The Digital Joneses

In 2026, the “Joneses” aren’t just your neighbors; they are influencers on your screen showing a curated, unrealistic version of life.

-

The Trap: You are comparing your “Behind-the-Scenes” to everyone else’s “Highlight Reel.”

-

The Hack: Practice Stealth Wealth. Find pride in what you have (your net worth) rather than what you show (your car or clothes). Real wealth is quiet; insecurity is loud.

Summary: The Mindset Shift Table

| Poor Mindset (Reactive) | Wealthy Mindset (Proactive) |

| Saving is a sacrifice. | Saving is buying freedom. |

| I’ll save whatever is left at the end of the month. | I pay myself first through automation. |

| I deserve a treat because I worked hard. | I deserve a stress-free future because I worked hard. |

| What will people think if I don’t buy this? | How much will this grow in 20 years? |

| Money is for spending. | Money is a tool for building a legacy. |

Discipline is a Skill, Not a Gift

Reprogramming your mind to save money isn’t an overnight event; it’s a series of small, intentional shifts in how you view the world. By understanding your biological biases, creating friction for bad habits, and connecting with your future self, you move from being a victim of your impulses to being the architect of your own wealth.

Discipline is like a muscle—the more you use it by making small, smart choices, the stronger it becomes. Start by automating one small transfer today. Your future self is waiting to thank you for the freedom you are currently building.