Why Discipline Is More Important Than Income

In the world of personal finance, we are often led to believe that a “high income” is the ultimate solution to all our problems. We tell ourselves, “If only I made six figures,” or “If I could just get that 20% raise, I’d finally be able to save.” We view income as the destination, assuming that wealth is a natural byproduct of a large paycheck.

However, as we navigate the economic complexities of 2026, the data tells a much different story. We are seeing a rise in “HENRYs” (High Earners, Not Rich Yet)—individuals making $250,000 a year who are still living paycheck to paycheck. Simultaneously, we see stories of librarians and janitors who leave behind multi-million dollar estates.

The difference between these two groups isn’t their salary; it’s their discipline.

Income is simply the fuel you put into your financial engine. If the engine is broken—if you have no discipline—it doesn’t matter how much fuel you pump in; the car isn’t going to get you to your destination. In this comprehensive guide, we will explore why discipline is the true architect of wealth and how you can master your behavior to achieve financial freedom, regardless of your current tax bracket.

The High-Income Trap: Why More Money Doesn’t Equal More Wealth

There is a massive psychological difference between Income and Wealth. Income is what you receive today for your labor; wealth is what you keep and grow for tomorrow.

The “High-Income Trap” occurs when an increase in earnings leads to a proportionate (or even greater) increase in spending. This is a psychological phenomenon where your “wants” quickly transform into “needs.” When you move from a $50,000 salary to a $100,000 salary, your brain tells you that you “need” a better car, a larger apartment, and more expensive vacations to match your new status.

The Reality of the “Golden Handcuffs”

Many high earners find themselves trapped in “Golden Handcuffs.” They have high-paying jobs but also have massive mortgages, luxury car leases, and private school tuitions. Because they lack the discipline to cap their spending, they are essentially one missed paycheck away from disaster. They have a high standard of living, but zero financial margin.

Parkinson’s Law and Your Bank Account: How Expenses Rise to Meet Income

To understand why discipline is superior to income, we must look at Parkinson’s Law. Originally coined to describe bureaucracy, it perfectly applies to personal finance: “Expenses rise to meet income.”

Without a disciplined system, your spending will naturally expand to consume every dollar you earn. If you make $3,000 a month, you’ll find a way to spend $3,000. If you get promoted and make $5,000, you’ll suddenly find that your “cost of living” has miraculously risen to $5,000.

Breaking the Cycle

Discipline is the only force capable of breaking Parkinson’s Law. It is the ability to say “no” to a lifestyle upgrade even when you can “afford” it. Wealth is built in the gap between your income and your expenses. If that gap is zero, your wealth is zero, no matter how many zeros are on your paycheck.

The Power of the Savings Rate: The Only Number That Truly Matters

In behavioral finance, we often talk about the Savings Rate. This is the percentage of your income that you keep after all expenses are paid.

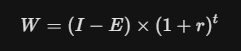

Mathematically, your savings rate is a much better predictor of your financial independence than your income level. Let’s look at the basic Wealth Equation:

Where:

-

W = Wealth

-

I = Income

-

E = Expenses

-

(I – E) = Your Discipline Gap (Savings)

-

r = Rate of return

-

t = Time

Notice that if (I – E) is zero, the entire equation collapses to zero. It doesn’t matter if I is $10,000 or $1,000,000; without the discipline to keep (I – E) positive, the power of compounding (r and t) has nothing to work with.

A Tale of Two Investors

-

Investor A: Earns $200,000/year, spends $195,000. Savings: $5,000/year.

-

Investor B: Earns $60,000/year, spends $45,000. Savings: $15,000/year.

Investor B is building wealth three times faster than Investor A, despite making less than a third of the income. That is the power of discipline over raw earnings.

Behavioral Finance: The Psychology of Discipline vs. Impulse

Why is discipline so hard? It’s because our brains were evolved for a world of scarcity, not the world of 2026 abundance. We are biologically wired for Hyperbolic Discounting—the tendency to choose a small reward now over a large reward later.

The Marshmallow Test of Finance

You’ve likely heard of the famous “Marshmallow Test,” where children were told they could have one marshmallow now or two if they waited. The children who waited tended to have better life outcomes.

Investing is essentially a lifelong Marshmallow Test. Discipline is the “muscle” that allows you to delay gratification. Every time you choose not to buy that impulse item on Amazon, you are choosing “two marshmallows” in the form of a stress-free retirement or the ability to leave a job you hate.

Avoiding the “Social Proof” Trap and Stealth Wealth

A major drain on income is the need for Social Proof. We use our spending to signal our success to others. This is often called “Keeping Up with the Joneses.”

The Paradox of the Millionaire Next Door

Most real millionaires don’t “look” like millionaires. They drive used Toyotas, live in modest neighborhoods, and shop at discount stores. This is “Stealth Wealth.” Their discipline allows them to ignore the social pressure to perform “richness.”

The trap of high income is that it often comes with social expectations. If you are a high-level executive, there is pressure to wear certain clothes or belong to certain clubs. It takes immense discipline to prioritize your Net Worth over your Network’s Opinion. Remember: You can either be rich or look rich. Rarely can you do both at the start of your journey.

Discipline in Debt Management: Turning the Tide of Interest

Income can buy you things, but only discipline can protect you from Interest. High earners often fall into the trap of using their income to “service” debt rather than build assets.

Interest: The Double-Edged Sword

-

Without Discipline: You pay interest (Credit cards, car loans, high-interest personal loans). This is a “tax” on your future self.

-

With Discipline: You earn interest (Dividends, compound growth, rental income). This is a “gift” to your future self.

A disciplined person with a low income will prioritize paying off a 20% interest credit card because they understand the math. An undisciplined person with a high income will just pay the “minimum” because they have the cash flow to cover it, not realizing they are bleeding wealth every month.

Compounding: The Reward for Financial Consistency

The “magic” of compound interest doesn’t require a high income; it requires Time and Consistency.

If you invest $500 a month with discipline for 30 years, you will likely end up a millionaire. If you invest $5,000 a month sporadically because you keep “needing” the money for lifestyle upgrades, you might end up with less.

The Volatility of Impulse

The market is volatile, but the biggest risk to your portfolio isn’t a market crash—it’s you. Discipline allows you to stay invested during the “Bear Markets” when everyone else is panicking. High income provides the opportunity, but discipline provides the staying power.

How to Build Financial Discipline: Actionable Steps for 2026

If you feel like you lack the discipline to grow your wealth, don’t worry. Discipline is a skill that can be built. Here are four strategies to “force” discipline into your life:

1. Automate Your Savings (The “Invisible” Discipline)

If you have to make a choice every month to save, you will eventually fail. We all have weak moments. The solution? Automate it. Set up a transfer that moves money from your paycheck to your investment account before you even see it. This is “The Pay Yourself First” rule.

2. The 24-Hour Rule

Before any non-essential purchase over $100, wait 24 hours. Most impulse buys are driven by a temporary dopamine spike. By waiting, you allow your rational brain to take over from your impulsive brain.

3. Track Your “Real” Hourly Wage

Calculate how much you actually take home after taxes and work-related expenses. Then, divide that by the hours you work. When you see that a new pair of shoes costs 10 hours of your life, you’ll find it much easier to be disciplined.

4. Focus on the “Big Three”

Don’t worry about the $5 latte if it stresses you out. Instead, be disciplined about the “Big Three”: Housing, Transportation, and Food. If you can keep these three costs low, you have already won 80% of the battle.

Summary: Income is the Tool, Discipline is the Craftsman

| Feature | High Income (No Discipline) | Low Income (With Discipline) |

| Spending | Increases with raises | Controlled/Purposeful |

| Debt | Used for lifestyle | Used strategically or avoided |

| Wealth | Visible but fragile | Invisible but robust |

| Stress | High (Running to stay still) | Low (Peace of mind) |

| Retirement | Dependent on high earnings | Driven by compound growth |

The Final Verdict

Income is great. We should all strive to increase our value to the marketplace and earn more. But income without discipline is a leaky bucket. You can pour as much water in as you want, but the bucket will never be full.

Discipline is what turns income into wealth. It is the quiet, daily commitment to your future self. It is the understanding that true freedom isn’t the ability to buy whatever you want; it’s the ability to not have to work if you don’t want to.

Stop waiting for a “life-changing” raise to start your financial journey. Start building the muscle of discipline today with whatever you have. Because in the end, it’s not about how much you make—it’s about how much you keep.