How to Reach Financial Independence Through Investing

The dream of “walking away” from a 9-to-5 job is no longer a privilege reserved for the ultra-wealthy or lottery winners. In the landscape of 2026, the tools, information, and markets required to achieve Financial Independence (FI) are more accessible to the average person than ever before.

But here is the cold, hard truth: Financial independence isn’t about “hitting it big” on a single stock or finding a secret crypto coin. It is a calculated, disciplined process that relies on mathematics, time, and psychology. If you want to reach a point where your investments pay for your life, you need a blueprint that goes beyond the surface.

In this comprehensive guide, we will break down the mechanics of wealth building, from the foundational math to the advanced psychological strategies required to stay the course.

Defining Financial Independence: More Than Just a “Big” Number

Most people confuse “being rich” with “being financially independent.” You can earn $500,000 a year and still be a slave to your desk if your expenses are $450,000.

Financial Independence is the moment your passive income from investments covers your living expenses. It is the transition from working for money to having your money work for you. In the “FIRE” (Financial Independence, Retire Early) community, this is often described as reaching your “FI Number.”

The Difference Between FI and Retirement

Traditional retirement is age-based. Financial independence is math-based. When you are financially independent, work becomes optional. You might choose to keep working because you find meaning in it, but the “need” for a paycheck is gone. This provides a level of psychological freedom that is arguably the greatest luxury money can buy.

The Core Mathematics of FI: The 4% Rule and Your “FI Number”

To reach financial independence, you must first know where the finish line is. Fortunately, there is a simple mathematical rule used by financial planners worldwide to determine this: The 4% Rule.

Understanding the 4% Rule

Based on the “Trinity Study,” researchers found that an investor could historically withdraw 4% of their portfolio’s initial value (adjusted for inflation) every year for 30+ years without running out of money.

How to Calculate Your FI Number

To find your number, follow this simple formula:

-

Calculate your annual expenses. (e.g., $50,000/year).

-

Multiply that number by 25.

In this scenario, $1.25 million is your “crossover point.” Once your portfolio hits this mark, you are technically financially independent.

Defensive Finance: Eliminating Debt and Building a Safety Net

You cannot build a skyscraper on a swamp. Before you put a single dollar into the stock market, you must secure your foundation.

The “Anti-Investment”: High-Interest Debt

If you have credit card debt at 20% interest, and the stock market historically returns 10%, you are losing 10% every year you don’t pay off that card. Paying off high-interest debt is a guaranteed return. It is the most profitable “investment” you will ever make.

The Emergency Fund: Your “Stay-in-the-Game” Insurance

The stock market is volatile. If an emergency happens (medical bill, car repair) and you are forced to sell your stocks while the market is down, you have permanently destroyed your compounding potential.

-

Target: 3–6 months of living expenses in a High-Yield Savings Account (HYSA).

This fund isn’t meant to make you rich; it’s meant to keep you from becoming poor.

Strategic Asset Allocation: Building Your Wealth Engine

Once your foundation is set, it’s time to choose the “engine” that will drive you to FI. For 90% of investors, the most efficient engine is a diversified portfolio of stocks and bonds.

The Power of Low-Cost Index Funds

In the past, you needed to pick individual stocks to get rich. Today, we know that most professional fund managers fail to beat the S&P 500 over the long run. By buying a Total Stock Market ETF (like VTI) or an S&P 500 ETF (like VOO), you own a piece of the most successful companies in the world.

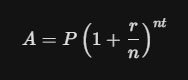

The Mathematics of Compounding

The “magic” of investing is the compound interest formula:

Where:

-

A: The future value of the investment.

-

P: The principal (the money you start with).

-

r: The annual interest rate (e.g., 0.08 for 8%).

-

t: The number of years.

The most important variable in this equation isn’t $r$ (the return); it is t (time). Because t is the exponent, the longer you stay invested, the more vertical the wealth curve becomes.

Tax-Advantaged Investing: Keeping More of What You Earn

If you want to reach FI faster, you have to stop giving your money to the government unnecessarily. In the United States and many other developed nations, the government provides “buckets” that allow your money to grow tax-free or tax-deferred.

1. The Roth IRA (The Holy Grail)

With a Roth IRA, you contribute after-tax money, but the money grows tax-free, and your withdrawals in retirement are completely tax-free. If you invest $100,000 and it grows to $1,000,000, that $900,000 gain is yours to keep, untouched by the IRS.

2. The 401(k) and Employer Match

If your employer offers a 401(k) match, that is an immediate 100% return on investment. Before you do anything else, ensure you are capturing every penny of that match. It is the only “free lunch” in the financial world.

The Silent Wealth Killers: Managing Inflation and Fees

Even a perfect investment strategy can be derailed by two silent predators: Inflation and Investment Fees.

The Inflation Hurdle

If the market returns 10% but inflation is 4%, your “Real Return” is only 6%. This is why sitting in “safe” cash is actually risky over the long term—inflation will slowly liquidate your purchasing power. To reach FI, your assets must outpace inflation.

The Impact of Expense Ratios

Many financial advisors and mutual funds charge a 1% or 2% fee. This sounds small, but over 30 years, a 1% fee can eat up nearly 25–30% of your final portfolio value.

-

Rule: Stick to index funds with “Expense Ratios” below 0.10%.

Behavioral Finance: Mastering the Psychology of the Market

Investing is $20% math and $80% behavior. The reason most people fail to reach financial independence isn’t because they weren’t “smart” enough; it’s because they weren’t “disciplined” enough.

The Danger of FOMO (Fear of Missing Out)

When your neighbor tells you they made a fortune on a meme stock or a speculative AI play, your brain releases dopamine. You feel the urge to jump in. This usually happens at the top of the market. Success in FI requires the ability to stay “boring” while everyone else is chasing hype.

Loss Aversion and Panic Selling

Psychologically, the pain of a loss is twice as intense as the joy of a gain. When the market drops 20% (which it does every few years), the “flight” instinct kicks in. The people who reach FI are the ones who view market crashes as “sales” and continue to buy when everyone else is selling.

Passive Income Streams: Diversifying Beyond the Stock Market

While the stock market is the most accessible path, true financial independence is often reinforced by multiple streams of income. This creates “antifragility”—if one market fails, another supports you.

1. Real Estate and REITs

Physical real estate offers leverage (using the bank’s money to buy an asset) and tax advantages. If you don’t want to be a landlord, REITs (Real Estate Investment Trusts) allow you to earn rental income through the stock market.

2. Digital Assets and Content

In 2026, digital real estate is a valid FI strategy. Websites, online courses, and automated YouTube channels can provide high-margin passive income that requires little capital but significant “sweat equity” to build.

3. High-Yield Dividend Stocks

As you get closer to your FI number, you may shift your portfolio toward “Dividend Aristocrats”—companies that have increased their dividends for 25+ consecutive years. This turns your portfolio into a “paycheck machine” that distributes cash without you ever having to sell your shares.

The 2026 Roadmap: A Step-by-Step Action Plan

Ready to start? Here is your “layman’s” roadmap to freedom:

-

Calculate Your Number: Multiply your annual expenses by 25.

-

Kill the Dragons: Pay off any debt with an interest rate above 7%.

-

Build the Moat: Save 3–6 months of expenses in a high-yield account.

-

Automate the Engine: Set up a recurring monthly transfer into a low-cost S&P 500 or Total Market Index Fund.

-

Maximize the Buckets: Fill up your 401(k) and Roth IRA before using a taxable brokerage.

-

Ignore the Noise: Stop checking your balance every day. Focus on your “Savings Rate” (the percentage of your income you save).

Freedom is a Choice, Not a Chance

Reaching financial independence through investing is not a sprint; it is a marathon of discipline. It requires you to prioritize your “future self” over your “present self.”

The truth is, the market is a wealth-generating machine that is open to everyone. It doesn’t care about your background, your degree, or your job title. It only cares about how much you invest and how long you stay.

Start today. Even if it’s just $50 a month, start the engine of compound interest. Your 65-year-old self (or your 40-year-old self) will thank you for the courage to begin.