Understand how bad habits can affect your financial life

Most people believe that financial success is a result of a few major life decisions: choosing the right career, landing a high-paying job, or making a lucky investment. While those factors certainly play a role, true financial stability—or ruin—is actually built in the quiet, repetitive moments of your daily life. It is built through your habits.

Habits are the invisible architects of our lives. They are the automated routines that our brains perform to save energy. However, when these routines are poorly calibrated, they act like a slow leak in a massive ship. You might not notice the water rising day by day, but eventually, the weight becomes too much to bear, and the ship sinks. In the world of personal finance, these “leaks” are bad habits that quietly drain your bank account, erode your credit score, and steal your future freedom.

To reclaim your financial life, you must first understand the psychological mechanisms of these habits and precisely how they impact your bottom line.

The Psychology of the Habit Loop: Why Your Brain Loves Spending

Before we can fix the behavior, we must understand the neurology behind it. Every habit, whether it is checking your phone or tapping your credit card for a “little treat,” follows a three-part neurological pattern known as the Habit Loop.

1. The Cue

The cue is the trigger that tells your brain to go into automatic mode. It could be an emotion (stress after a long meeting), a time of day (the 3:00 PM energy slump), or a location (walking past your favorite coffee shop).

2. The Routine

This is the behavior itself. In a financial context, the routine is the act of spending: ordering delivery, browsing an online sale, or saying “yes” to an expensive dinner you hadn’t planned for.

3. The Reward

The reward is the hit of dopamine your brain receives. It’s the temporary relief from stress, the excitement of a new purchase, or the social validation of fitting in. Because the brain loves this reward, it reinforces the loop, making the behavior more likely to happen next time you encounter the cue.

The danger of bad financial habits is that the reward is immediate, while the consequence (debt, lack of savings) is delayed. Our primitive brains are wired to prioritize “now” over “later,” which is why financial discipline feels so difficult.

The High Price of Convenience: How Modern Apps Drain Your Savings

In 2026, we live in a “frictionless” economy. Companies have spent billions of dollars removing every possible barrier between you and your money. While convenience is a luxury, it often becomes a destructive habit that eats away at your disposable income.

The Delivery Trap

Services like DoorDash, Uber Eats, and Instacart have transformed from “emergency options” into daily habits for many households. What looks like a $15 meal often turns into a $30 expense once you add delivery fees, service charges, and tips. If this happens three times a week, you are spending nearly $2,400 a year just on the convenience of having food brought to you.

Subscription Creep

The “subscription model” is designed to exploit the habit of forgetfulness. Whether it is streaming services, “premium” apps, or monthly “mystery boxes,” these $9.99 or $14.99 charges seem insignificant. However, the habit of signing up and never auditing your subscriptions leads to “leakage.” It is not uncommon for the average consumer to discover they are spending over $200 a month on services they rarely use.

Frictionless Payments

Biometric payments (FaceID and thumbprints) have removed the “pain of paying.” When you had to physically count out cash, your brain registered the loss of a resource. Now, spending is a seamless digital gesture. The habit of “one-click” buying bypasses the analytical part of your brain, leading to a higher volume of impulsive purchases.

Understanding the “What-The-Hell” Effect in Personal Finance

Psychologists use a term called the “What-The-Hell Effect” to describe the cycle of indulgence, regret, and further indulgence. It is a major contributor to financial ruin.

Imagine you have a budget for the month. On the second week, you accidentally overspend by $50 on a night out. Instead of adjusting your spending for the rest of the month, your brain says, “Well, I’ve already ruined my budget for this month, so what the hell, I might as well buy those shoes I wanted.”

This habit of “all-or-nothing” thinking leads to massive financial swings. It transforms a minor slip-up into a catastrophic month. To build wealth, you must replace the “What-The-Hell” habit with “Damage Control.” Financial success isn’t about being perfect; it’s about how quickly you can get back on track after a mistake.

The Impact of Bad Habits on Your Credit Score and Future Borrowing

Bad habits don’t just affect your current cash flow; they damage your reputation in the eyes of financial institutions. Your credit score is essentially a “grade” on your financial habits.

The Minimum Payment Trap

One of the most damaging habits is paying only the minimum balance on credit cards. This habit signals to your brain that the debt is “handled,” but mathematically, it ensures you stay in debt for decades.

Consider a $5,000 balance on a card with 20% APR. If you only pay the minimum, you could end up paying over $10,000 in interest alone and taking 20 years to pay it off. This habit turns a temporary purchase into a permanent anchor on your wealth.

Habitual Late Payments

Even being a few days late on a bill—due to disorganization or procrastination—can have a staggering impact. A single 30-day late payment can drop a high credit score by 60 to 100 points. This habit of “financial disorganization” increases the interest rates you’ll pay on future mortgages and car loans, costing you tens of thousands of dollars over your lifetime.

Opportunity Cost: The Hidden Price Tag of Every Small Purchase

To a disciplined mind, the cost of a bad habit isn’t just the dollar amount on the receipt; it is the opportunity cost. Every dollar spent on a bad habit is a dollar that cannot be invested to grow.

The Power of the “Coffee Factor” Updated

While the “don’t buy lattes” advice is often mocked, the math behind it remains undeniable when applied to any recurring bad habit. If you spend $20 a day on “little extras” (convenience food, snacks, impulse digital purchases), that totals $600 a month.

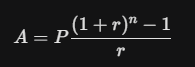

If you invested that $600 a month into a diversified index fund with an average 8% annual return, look at what happens over time:

-

In 10 years: You would have ~$110,000.

-

In 20 years: You would have ~$350,000.

-

In 30 years: You would have nearly $900,000.

The bad habit isn’t just costing you $20 a day; it is costing you nearly a million dollars in retirement. When you view habits through the lens of compound interest, “small” expenses suddenly look very large.

Social Habits: The Danger of “Keeping Up with the Joneses”

In the age of social media, our social habits have become more expensive than ever. We are constantly exposed to the “highlight reels” of our friends and influencers, leading to a subconscious pressure to match their lifestyle.

Comparison Spending

The habit of comparing your life to others’ leads to “status spending.” You buy the latest iPhone, the trendy sneakers, or the expensive vacation not because they bring you joy, but because you don’t want to appear “behind.”

The “Yes-Man” Social Habit

Many people struggle with the habit of saying “yes” to every social invitation. Whether it is an expensive brunch, a destination wedding, or a weekend trip, the fear of missing out (FOMO) overrides financial logic. Developing the habit of saying, “That sounds fun, but it’s not in my budget this month,” is one of the most powerful moves you can make for your net worth.

Breaking the Cycle: Strategies to Rewire Your Financial Brain

The good news is that habits are not permanent. Because they are learned behaviors, they can be unlearned. However, you cannot rely on willpower alone. Willpower is like a muscle—it gets tired by the end of the day. Instead, you must use systems.

1. Introduce Friction

Companies spend billions removing friction; you must put it back.

-

Delete shopping apps from your phone so you have to use a computer to buy anything.

-

Unsubscribe from marketing emails so you aren’t triggered by “sales.”

-

Remove saved credit card info from your browser so you have to physically find your wallet to make a purchase.

2. The 24-Hour Rule

Make it a non-negotiable habit to wait 24 hours before any purchase over $50. This “cool-down” period allows the dopamine spike to subside and the rational part of your brain (the prefrontal cortex) to take back control.

3. Automate the Good Habits

If you struggle with the habit of saving, take the decision out of your hands. Set up an automatic transfer that moves money to your savings or investment account the same day your paycheck hits. If you never see the money, you won’t miss it. This turns “saving” from a difficult choice into an automated background process.

The Compounding Effect of Good Habits

Just as bad habits compound to create ruin, good habits compound to create wealth. Financial freedom is rarely the result of a single “big win.” It is the result of hundreds of small, seemingly insignificant choices made correctly over time.

-

The habit of tracking your net worth once a month.

-

The habit of reading ten pages of a financial book every day.

-

The habit of checking your bank statement weekly for errors or unused subscriptions.

-

The habit of negotiating your bills once a year.

These actions take very little time, but over a decade, they build a psychological “armor” that protects you from the consumerist culture around you.

You Are Your Habits

Your current financial situation is a lagging indicator of your past habits. If you want to change your destination, you must change the direction you are heading in every single day.

Stop looking for the “magic stock” or the “perfect side hustle” to save you. Instead, look at your daily routine. Look at the $10 here and the $20 there. Look at how you respond to stress, boredom, and social pressure. By mastering your habits, you aren’t just saving money—you are buying back your time, your peace of mind, and your future.

Start small. Pick one bad habit—just one—and commit to replacing it with a better system this week. Your future self is counting on it.