What is a credit card annual fee and when is it worth it?

For most people, opening a credit card statement and seeing a surprise charge for $95, $250, or even $695 can be a jarring experience. This charge, known as the annual fee, often feels like a penalty for simply having an account. In an era where “No Annual Fee” cards are advertised on every corner, paying a bank for the privilege of using their plastic seems counterintuitive.

However, in the competitive world of personal finance, an annual fee isn’t just a cost—it is a membership fee. Just as you pay for a warehouse club membership to access lower prices, or a streaming service for exclusive content, premium credit cards charge an annual fee to unlock a suite of benefits that can, if used correctly, far outweigh the initial expense.

Understanding the math behind the “break-even point” is the difference between wasting money on a status symbol and strategically using a financial tool to save thousands of dollars every year.

What Exactly Is a Credit Card Annual Fee?

At its simplest, an annual fee is a once-a-year charge that a credit card issuer levies on a cardholder to keep the account active. It is usually charged on your first statement after opening the card and then every 12 months on your “anniversary” date.

While many entry-level cards have a $0 annual fee, “Premium” and “Ultra-Premium” cards use these fees to fund the high-end rewards they offer. The fee is effectively the “entry price” for access to higher cash-back rates, travel points, and luxury perks that the bank could not otherwise afford to provide for free.

How the Fee Is Charged

Most banks charge the fee in one lump sum. However, if you decide the card isn’t for you, most issuers offer a 30-day window after the fee posts to cancel the card and receive a full refund.

Why Banks Charge Annual Fees: The Business Behind the Benefit

It is a common misconception that banks charge annual fees simply to increase their profit margins. While that is part of the equation, the primary reason is to offset the cost of high-value benefits.

A “No Annual Fee” card typically offers basic rewards (like 1% or 1.5% cash back) because the bank earns enough from “interchange fees” (the percentage merchants pay when you swipe) to cover those costs. But when a card offers 4% or 5% back on specific categories, plus airport lounge access and travel insurance, the interchange fees aren’t enough. The annual fee bridges that gap.

The Target Audience

Banks use annual fees to filter for “high-spend” or “loyal” customers. Someone willing to pay a $250 fee is likely to use that card as their primary payment method, providing the bank with more data and more transaction volume.

Annual Fee vs. No Annual Fee: Which One Is Better for You?

The “better” card depends entirely on your spending habits and lifestyle. There is no one-size-fits-all answer, but there are clear indicators for each path.

When to Choose a No Annual Fee Card

-

You are a light spender: If you only spend a few hundred dollars a month, you likely won’t earn enough rewards to cancel out a fee.

-

You want simplicity: You don’t want to track “statement credits,” “airline incidentals,” or “lounge locations.”

-

You are building credit: If you are just starting out, keeping a $0 fee card open forever is the best way to increase your “length of credit history” without any cost.

When to Choose a Premium Card (With a Fee)

-

You travel at least twice a year: Travel perks like checked bag waivers and lounge access can pay for the fee in just one trip.

-

You have high expenses in specific categories: If you spend $1,000 a month on groceries, a card with a $95 fee that gives 6% back is much better than a $0 fee card that gives 1% back.

-

You already use the services the card credits: If a card costs $250 but gives you $240 in “Uber Credits” that you would have spent anyway, the card effectively costs you only $10.

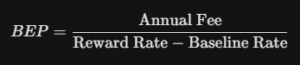

How to Calculate the “Break-Even Point” of a Credit Card

To decide if a card is worth it, you need to move beyond emotions and look at the math. We use a simple formula to find the Break-Even Point ($BEP$).

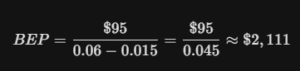

For example, imagine a card has a $95 annual fee and offers 6% back on groceries. Your alternative (baseline) is a free card that offers 1.5% back.

In this scenario, if you spend more than $2,111 per year ($176 per month) on groceries, the card with the annual fee is mathematically superior to the free card. Every dollar you spend above that amount is pure profit compared to using a free card.

The Hidden Value: Perks That Can Outweigh the Fee

The biggest mistake people make is only looking at the “points” or “cash back.” Premium cards often include “tangible credits” that act like cash.

1. Travel Statement Credits

Many high-end cards offer an annual “Travel Credit.” For instance, a card might have a $550 fee but offer a $300 credit that is automatically applied to any travel purchase (hotels, flights, taxis). This immediately reduces the “effective” cost of the card to $250.

2. Subscription and Lifestyle Credits

Modern cards now offer monthly credits for services like:

-

Streaming services (Hulu, Disney+, Netflix)

-

Ride-sharing (Uber, Lyft)

-

Food delivery (DoorDash, UberEats, Grubhub)

-

Fitness (Equinox, Peloton)

If you already pay for these services, the credit is “as good as cash.” If you don’t use them, the credit is worth zero.

3. Airport Lounge Access

A single-day pass to a premium airport lounge usually costs around $50. If you and a guest visit a lounge four times a year, that is $400 in value. For a frequent traveler, this perk alone justifies almost any annual fee.

4. Global Entry / TSA PreCheck Credits

Most cards with fees over $95 offer a credit (usually $100) every four years to cover the application fee for Global Entry or TSA PreCheck.

Luxury Benefits: Protecting Your Finances and Your Time

Beyond the dollar-for-dollar credits, annual fee cards offer “Soft Benefits” that provide insurance and peace of mind. These are often overlooked until something goes wrong.

-

Primary Rental Car Insurance: Most free cards offer “secondary” insurance. Premium cards often offer “primary” insurance, meaning you don’t have to involve your personal car insurance if you have an accident in a rental.

-

Trip Delay and Cancellation Insurance: If your flight is canceled or delayed by more than 6 hours, these cards will reimburse you for hotels and meals (up to $500 per person).

-

Purchase Protection: If you buy a new iPhone and drop it or it gets stolen within 90 days, the card issuer may refund you the full cost.

-

Extended Warranty: Many cards add an extra year to the manufacturer’s warranty on electronics and appliances.

The “Retention Call”: How to Get Your Annual Fee Waived

One of the best-kept secrets in finance is that annual fees are often negotiable. Banks spend hundreds of dollars in marketing to acquire you as a customer. They do not want to lose you over a $95 or $250 fee.

When your annual fee posts, call the number on the back of your card and speak to the “Retention Department.” You can use a script like this:

“I’ve noticed the annual fee has posted to my account. I’ve enjoyed using the card, but I’m finding it hard to justify the cost this year compared to some other no-fee options I’m seeing. Is there anything you can do to help me keep the account open, such as a fee waiver or a bonus point offer?”

Possible Outcomes:

-

The Full Waiver: They simply remove the fee.

-

The Retention Offer: They offer you points (e.g., “Spend $1,000 in 3 months and we will give you 20,000 points”) that are worth more than the fee.

-

The Statement Credit: They offer a partial credit to lower the cost.

-

The Downgrade: If they offer nothing, you can “Downgrade” (Product Change) the card to a $0 fee version. This keeps your credit history intact without paying the fee.

Common Mistakes: When an Annual Fee Becomes a Bad Idea

While premium cards can be great, they can also be a trap if you aren’t careful. Avoid these three common pitfalls:

1. Chasing Perks You Don’t Use

Don’t pay for a card because it offers a “Saks Fifth Avenue Credit” if you never shop at Saks. A credit is only valuable if it offsets an expense you were already going to have.

2. Carrying a Balance

This is the golden rule: Never carry a balance on a rewards card. The interest rates on premium cards (often 24%+) will instantly wipe out any rewards or perks you earned. If you can’t pay in full every month, a “Low Interest” card without rewards is a much better choice.

3. Forgetting the Anniversary

If you have five different cards with annual fees, they can sneak up on you. Keep a simple spreadsheet or use a tracking app to know when your fees are due so you can decide whether to keep, cancel, or negotiate the card.

Is the Fee Worth It for You?

The annual fee is not a boogeyman; it is a calculation. To decide if a card belongs in your wallet, perform a “Year-End Audit.” Look at the total rewards you earned, add the value of the credits you used, and subtract the annual fee.

If the number is positive, you have a winner. If the number is negative, it’s time to downgrade. By treating your credit cards as a business ledger rather than just a way to pay, you can turn a yearly cost into a significant financial advantage.